Independent Market Monitoring

IMM uses trade flow analysis and market research to independently assess trade and market impacts of FLEGT Voluntary Partnership Agreements (VPAs) in the EU and partner countries.

DATA DASHBOARD

Explore up-to-date data on timber trade flows across the world

You can get a bird’s eye view on global timber trade! Plus, customize tables and charts for your own analysis.

Latest News

EU-Indonesia first half 2022 trade trends

Global export value of Indonesian timber and paper product grows 10% year-on-year Indonesia’s...

EU-VPA partner country trade overview – first half of 2022

In the first half of 2022 EU imports of timber and wood products from VPA partner countries grew...

FLEGT awareness raising key, say Ghana consultations

With the qualification that it could be better disseminated, Ghana timber sector stakeholders rate...

COUNTRY PROFILES

Access to the latest commentary

on timber industries and economies of EU and

VPA partner countries

Publications

VPA partner timber trade and market perceptions update

VPA partner timber trade and market perceptions update DOWNLOADS FULL REPORT CATEGORYModular...

VPA partner timber trade and market perceptions update

VPA partner timber trade and market perceptions update DOWNLOADS FULL REPORT CATEGORYModular...

FLEGT-licensed timber trade and market perceptions update

FLEGT-licensed timber trade and market perceptions update DOWNLOADS FULL REPORT CATEGORYModular...

FLEGT VPA Partners in EU Timber Trade 2020

FLEGT VPA Partners in EU Timber Trade 2020 DOWNLOADS FULL REPORT CATEGORYAnnual Report PUBLISHED...

Study of EU public timber procurement policies, private sector policies and related giudance

Study of EU public timber procurement policies, private sector policies and related giudance...

FLEGT VPA Partners in EU Timber Trade 2019

FLEGT-licensed timber in the EU market Full report, French Executive Summary, Bahasa...

WORKSHOPS

Meet our market analysts for informed decisions

Our workshops cover latest timber market trends, FLEGT VPA updates and more for government authorities, licensing bodies, timber producers, exporters and importers.

PAST EVENTS

Tropical trade trends and FLEGT profile

Tropical trade trends and FLEGT profile Tropical timber trade trends through the pandemic and the...

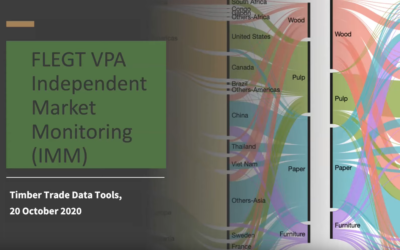

IMM timber trade data tools

IMM timber trade data tools Accurate and timely information on timber trade flows is crucial to...

Spanish Trade Consultation

Spanish Trade Consultation Gallery Presentations Workshop 1. Trends in the European tropical...

Subscribe to our newsletters

Subscribe to our newsletter feed and receive all the latest news

Our Partners

Funded by