More market mayhem

The situation in key EU sales markets for tropical timber and timber products has remained buoyant but tense in the first few months of 2022, according to IMM trade survey respondents, with demand frequently still exceeding supply, despite sharp price increases.

Companies sourcing timber and timber products in Southeast Asia and South America quoted high freight costs as the main reason for price hikes. Moreover, at least some suppliers were still working at reduced capacity and unable to satisfy additional orders, according to survey respondents. The situation in Africa was said to be a little easier, both where freight rates and timber supply are concerned. The strict lockdowns in several major Chinese cities have reportedly eased the competitive pressure on the procurement markets at least temporarily.

Until the end of the first quarter, survey respondents reported strong demand from the building, carpentry, renovation, and DIY sectors in key EU markets. At the same time, the supply situation had gradually improved and some respondents were expecting a more balanced market in the second quarter.

However, the war between Russia and Ukraine and European sanctions against Russia became another game changer in March and April.

Summer cool-down and deteriorating prospects

Economic sanctions against Russia have created a significant supply gap for the European timber and downstream industries, as a result of which prices continued to rise in the second quarter. While the Russian supply gap is creating considerable market opportunities for other producer countries, price inflation has now reached a critical level and in some countries construction companies as well as the DIY sector and private consumers are beginning to postpone projects and timber product purchases, said IMM survey respondents. In May, June, and July, demand for tropical timber products has slowed down noticeably as a result, with the exception of the Netherlands, where many respondents still reported strong demand.

Given the significant uncertainties caused by the war in Ukraine and economic sanctions, future developments are difficult to predict, even in the short term. Some survey respondents were expecting demand to pick up again soon, bolstered by government subsidies for thermal renovation projects and public investment in urgently needed housing developments.

Others were more guarded, especially where tropical timber is concerned. Private investment, in particular, was expected to focus more on basic necessities rather than luxury or “cosmetic” home repairs and improvements in the near future. At the same time, all players along the supply chain are expected to manage their stocks very carefully and wait as long as possible for prices to soften. As a result, many market players are expected to focus more on products with short and reliable supply chains and delivery times.

EU-VPA partner countries trade overview – first quarter of 2022

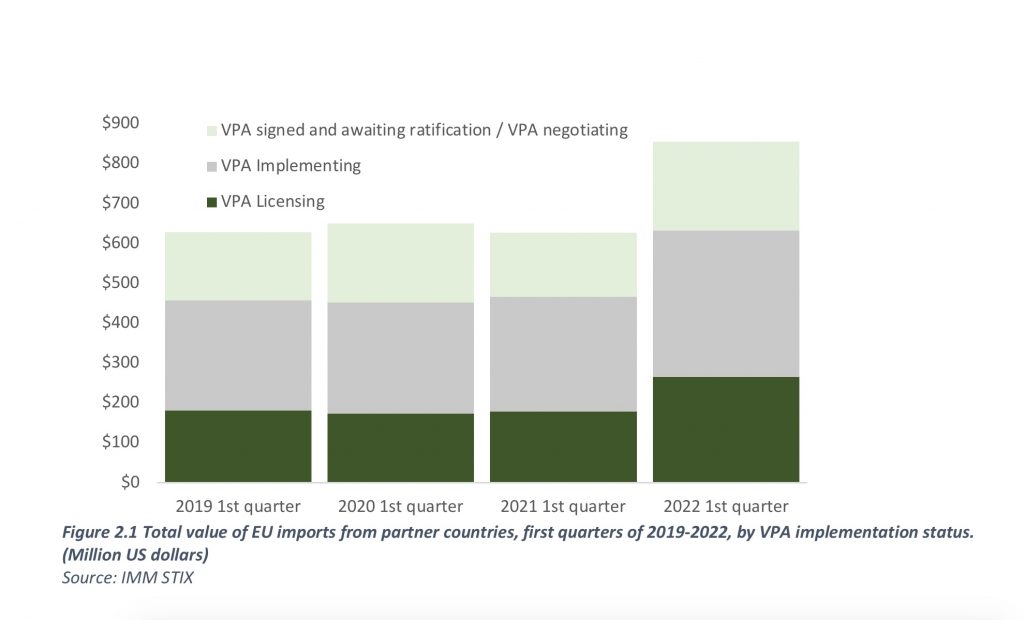

The total value of VPA partner countries timber products exports to the EU increased 36.1% to USD 854 million in the first quarter of 2022 following a 3.6% decline in the same period of 2021 where it was valued at less than USD 626 million. The total value of EU imports from VPA partner countries in the first quarter of 2022 stood 36% higher in value than it was in the equivalent period of the last pre-COVID year – 2019. Indonesia remains the only VPA partner country that that exports FLEGT Licensed products. [Figure 1.1]

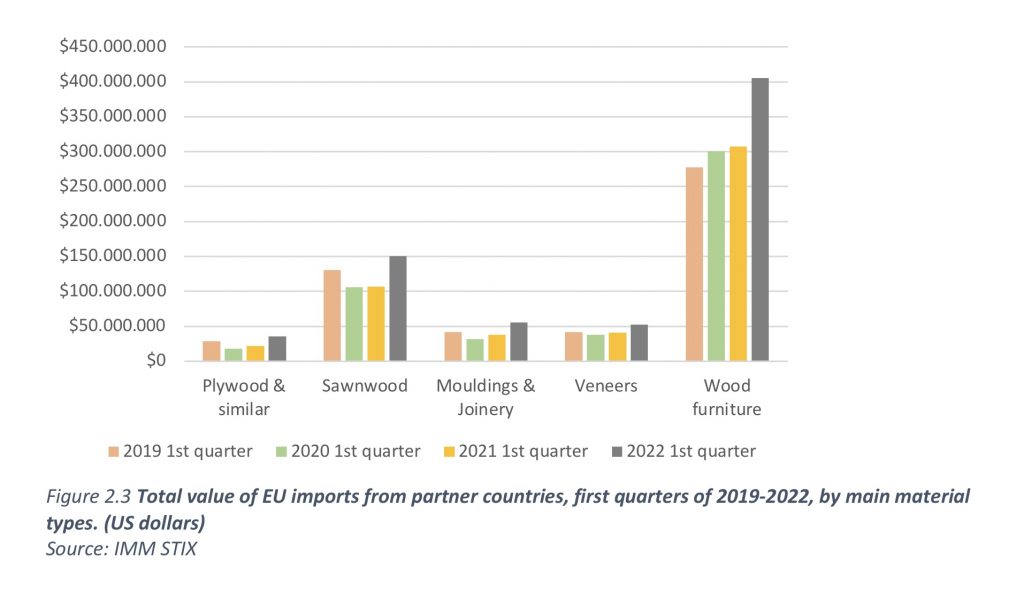

In the first quarter of 2022 wooden furniture continued to be the dominant product category imported by the EU from VPA partner countries. With a 32% value increase compared to the same quarter in 2021, and 46% growth compared to the same quarter in 2019, imports of wooden furniture to the EU from VPA partner countries amounted to USD 405 million in 2022.

Sawnwood continued to be the second largest material type in terms of value for imports to the EU from VPA partners in the first quarter of 2022. With imports valued at USD 150 million in the first quarter, this showed growth of 40% compared to the same quarter in 2021 and a 15% increase in value compared to 2019.

Wood mouldings and product imports to the EU from VPA partners grew by nearly 46% in value in the first quarter of 2022, compared to 2021. At a value of over USD 55 million, import value is nearly 34% higher than in the first quarter of 2019.

Veneer imports to the EU from VPA partner countries rose to USD 52 million in the first quarter of 2022. This represents nearly 29% growth compared to the same period in 2021 and nearly 25% compared to the first quarter of 2019.

Plywood imports by the EU from VPA partner countries grew by 62% in the first quarter of 2022 compared to 2021, and by 22% compared to the first quarter of 2019. With a value in the first quarter of 2022 of over USD 35 million, plywood and related materials are the fifth largest product group imported from VPA partner countries.