IMM’s overview of the current market situation for FLEGT Licensed and VPA partner timber products in the EU27 shows that the recovery has been stronger than expected on the demand side but supply side issues are constraining market growth. A rapid escalation in prices for VPA partner timber, driven by production and shipping constraints, extremely high freight rates, and a sharp and unexpectedly rapid increase in demand in global markets, has led to EU27 importers buying more from more accessible suppliers in the European neighbourhood. EU27 imports of FLEGT licensed timber from Indonesia, and of wood furniture and other finished products from Vietnam have recovered lost ground this year, but have continued to lose share to other suppliers, particularly in Russia and other CIS countries, Turkey, Bosnia Herzegovina, Serbia, and India. Meanwhile suppliers in African and Latin American VPA partner countries continue to operate under extremely challenging conditions and there has only been a weak uptick in EU27 imports from these countries in 2021 while their share of total EU27 imports of primary wood products continues to slide.

There are certainly more positive signs emerging on the demand side as the economic recovery in the EU gains momentum. This trend is expected to continue as vaccination rates are rising, lockdown measures are eased and the full effects of NextGenerationEU, the EU’s large fiscal stimulus programme, begin to be felt. According to the EU’s Summer 2021 Economic Forecast published in July, following a 6.0% decline in 2020, the EU economy is now forecast to expand by 4.8% in 2021 and by 4.5% in 2022. This represents a significant upgrade of the growth outlook compared to the Spring 2021 Economic Forecast which the Commission presented in May.

The contraction of EU GDP in the first quarter of this year turned out to be marginal and milder than expected. Upbeat survey results among consumers and businesses, as well as data tracking mobility, suggest that a rebound in EU27 consumption is well underway and set to strengthen in the coming months. There is also evidence of a revival in tourism activity, which should also benefit from the new EU Digital COVID Certificate. Together, these factors are expected to outweigh the temporary production input shortages and rising costs hitting parts of the manufacturing sector.

Economic growth rates will continue to vary across the EU. Some Member States (e.g. Germany, Netherlands, Sweden, Denmark, Poland) are now expected to see economic output return to their pre-pandemic levels by the end of 2021. Others (e.g. Spain, France, Italy, Portugal) will take longer, but all should see their economies return to pre-crisis levels before the end of 2022.

According to the EU’s forecast, uncertainty and risks surrounding the growth outlook are high but remain overall balanced. The threat posed by the spread and emergence of variants of concern underscores the importance of a further rapid increase in full vaccination. Economic risks relate in particular to the response of households and firms to changes in restrictions and the impact of emergency policy support withdrawal.

Forward looking indicators show that economic momentum in the EU27 has picked up since the start of the year, although business and consumer confidence is still quite fragile, particularly in the construction sector, a key driver of timber demand in the region. The IHS Markit Eurozone Construction Index rose from 49.5 in August to 50.0 in September, signalling a stabilisation in eurozone construction activity following two successive months of decline. Where activity rose, companies often cited stronger demand growth, although this was offset by a lack of raw materials which halted work on site. Underlying data indicated that growth was centred around house building, while commercial construction was steady but infrastructure activity was still slow. According to IHS Markit, construction firms were confident that activity will increase over the next 12 months amid forecasts of strengthening economic conditions, improved supplier performance and new projects.

Contrasting trends in EU27 imports of primary wood products

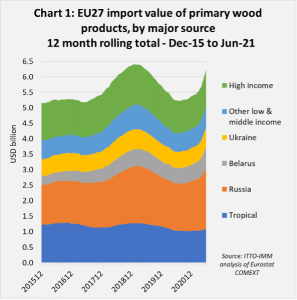

EU27 imports of primary wood products (logs, sawn, veneers and plywood) show contrasting trends when assessed on the basis of value (Chart 1) and quantity (Chart 2). Considering the long-term, the USD value of imports increased sharply in 2018 on the back of a rise in the value of the euro, alongside improved economic confidence and construction activity in the EU, but then fell sharply in the second half of 2019 as these trends reversed and there was severe overstocking in the plywood sector. The downturn deepened during the pandemic lockdowns in the second quarter of 2020. However the pandemic-induced downturn proved to be short-lived and was quickly offset by a sharp rise in spending on home and garden improvement by consumers whose movements were severely curtailed.

The combination of a sharp unexpected increase in demand and the supply side problems due to the pandemic led to a sharp rise in wood product prices from the last quarter of 2020. EU27 import prices were also pushed up by a worldwide shortage of containers raising freight rates. This is reflected in a very rapid increase in the total value of EU27 imports of primary wood products in the first half of 2021, particularly in imports from the Russian Federation. Further weakening of the Russian rouble helped increase the relative competitiveness of Russian softwood and plywood products during this period.

EU27 import value of primary wood products from tropical countries recovered more slowly in the first 6 months of this year. Tropical wood was disproportionately impacted by supply side problems during the pandemic, including the challenges of moving materials, staff and equipment to mills and very high freight rates in less accessible locations. In the 12 months to June 2021, the share of tropical countries in EU27 import value of primary wood products was only 17%, down from 20% in the previous twelve month period.

While the immediate cause of falling tropical primary product imports into the EU27 was slowing economic activity in 2019 and the disruption due to the pandemic in 2020, it also forms part of a long term trend of declining market share for tropical wood in these countries. The figure of 17% for tropical wood in EU27 import value of primary wood products is very likely the lowest ever recorded and compares to figures of around 40% prior to the global financial crises. Reasons most often cited for the decline in tropical wood market share at IMM trade consultations in the EU include: environmental prejudices; uncoordinated marketing of tropical wood products; substitution by temperate, chemically and thermally modified wood, composites and non-wood materials; and the challenges of demonstrating EUTR conformance in tropical countries in the absence of FLEGT-licensing.

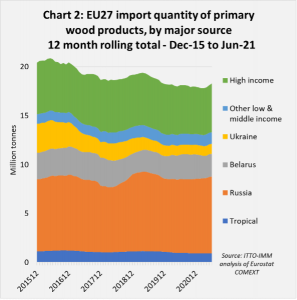

The trend in EU27 primary wood product imports looks different in quantity terms (Chart 2). The long term trend in import tonnage of primary products is downwards, a reflection primarily of measures to restrict log exports, particularly in CIS countries on the borders of the EU27 which has encouraged a switch to less bulky and higher value imports of semi-processed and finished wood products. Tropical primary products, which tend to be relatively high value, accounted for only around 5% of EU27 imports of primary wood products in quantity terms in the 12 months to June 2021, down from 6% in 2019.

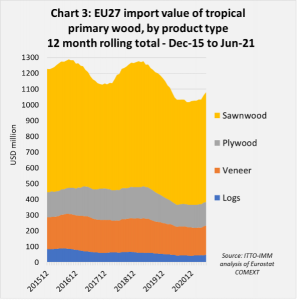

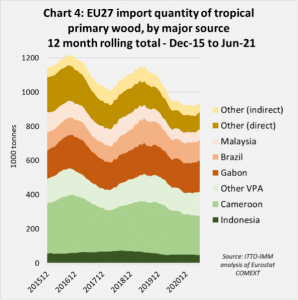

When considering just tropical primary wood products, recent trends in EU27 imports revealed by the value data (Chart 3) and quantity data are equivalent (Chart 4). Overall there has been volatility, particularly in imports of tropical sawnwood, but the general trend has been downward. This year, there has been a slight uptick in EU27 imports of tropical primary wood products, but this is in line with an existing cycle of rise and fall roughly every two years, with the dips tending always to be steeper than the upturns.

Closer analysis of the countries involved highlights the central position played by Cameroon as a key driver of the EU27 tropical wood import trend (Chart 4). However, this year there are signs that Cameroon is gradually being overhauled by Gabon. Cameroon accounted for 25% of all EU27 imports of tropical primary wood products (by quantity) in the 12 months to June 2021, down slightly from 27% in 2019. In the same period, Gabon’s share increased from 16% to 20%.

Considering the role of VPA partners, in total the nine tropical countries that have signed a VPA (a group which includes Cameroon but excludes Gabon) accounted for 45% of all EU27 imports of tropical primary wood products in the twelve months to June 2021, down from 47% in 2019. FLEGT licensed wood from Indonesia accounted for just 5% of EU27 tropical primary wood product imports in the twelve months to June 2021, the same proportion as in 2019.

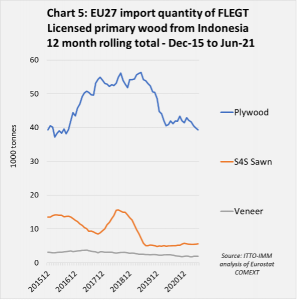

The relatively low proportion of tropical primary wood products that is FLEGT licensed is, however, partly due to Indonesia’s policy to restrict log and sawnwood exports. Of primary wood products, Indonesia exports only plywood, S4S (surfaced on 4 sides) sawnwood and veneer. In the 12 months to June 2021, the EU27 imported a total of 47,000 tonnes of these products from Indonesia, down from 49,000 tonnes in the previous twelve month period and from 56,000 tonnes in 2019.

EU27 imports of plywood from Indonesia increased alongside imports from other sources during the short-lived plywood boom in 2017 and 2018, and then declined in 2019 when the market started to suffer from severe over-stocking. EU27 imports have since stabilised at a level of around 40,000 tonnes a year, the same as the period just before the boom (and FLEGT licensing) began in 2016. Overall Indonesia has lost ground to Russian birch plywood in this market in the last two years. EU27 imports of Indonesian plywood were 34,400 cu.m in the first six months of 2021, 9% less than the same period in 2020 and 31% less than in 2019. This compares to EU27 imports of hardwood plywood from Russia which were 625,000 cu.m in the first six months of 2021, 13% more than the same period in both 2020 and 2019.

While EU27 imports of S4S sawnwood from Indonesia increased briefly in 2018, they then declined sharply in 2019 and have remained flat at a low level ever since. EU27 imports of veneer from Indonesia have continued to slide (Chart 5).

EU27 wood product imports from all other VPA partners are dominated by sawnwood, the leading VPA partner suppliers all being in Africa. Sourcing hardwood from tropical African countries has always been challenging and trade is typically volatile, with long lead times between placing of orders and delivery. These problems have become even more pronounced during the pandemic.

European importers, distributors and merchants of sawn hardwood interviewed for market reports in 2021 have highlighted that the trading environment has been like nothing they’ve experienced during decades in the business. Demand has climbed across key markets, while freight rates have reached unprecedented levels. Supply has become exceptionally tight and lead times have stretched from sources globally. Prices have consequently hit the heights, while margins for importers are variously described as good to extremely so. A key demand driver across the continent has been the boom in home improvement, refurbishment and DIY markets.

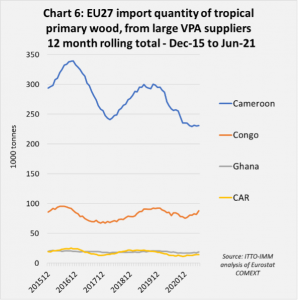

Against this background, the lack of any significant upturn in EU27 imports from VPA partners in Africa in the first six months of this year can only be explained by supply side problems. There has been a slight uptick in EU27 imports of tropical wood products from the Republic of Congo this year, but imports from Cameroon have remained slow, while those from Ghana and the Central African Republic have been flat at a low level (Chart 6).

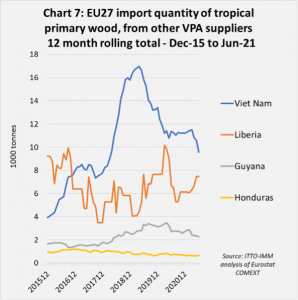

EU27 imports of primary wood products from other VPA partners are very limited and have been extremely volatile in recent years (Chart 7). The EU27 imports a small quantity of plywood and sawnwood from Vietnam, but volumes have fallen away sharply since 2018 when they briefly peaked at 16,000 tonnes. Imports from Liberia, nearly all logs destined for France, have been intermittent but flat overall, continuing to average around 7000 tonnes a year, both before and during the pandemic. EU27 imports from Guyana, a mix of logs and sawnwood, increased slowly between 2016 and 2019 to reach around 3000 tonnes but fell to little more than 2000 tonnes in the 12 months to June 2021. Imports from Honduras, always negligible, have been sliding downwards for the last 5 years.

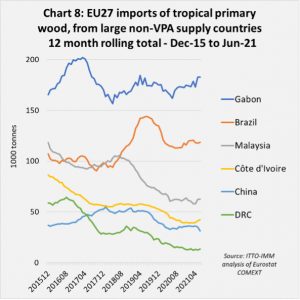

Imports of tropical primary wood products have also been sliding from most non-VPA countries. Imports of these products from Malaysia, Cote d’Ivoire, China and DRC, began to weaken at the start of 2019, well before the onset of the pandemic. The exceptions are Gabon and Brazil. Although imports from Gabon weakened in 2017, they have been gradually recovering ever since and now comprise a good mix of sawnwood and veneer, with plywood also making gains. Imports of tropical primary wood products from Brazil, now almost entirely comprising sawnwood (nearly all plywood imports from Brazil are softwood and non-tropical hardwood), have been extremely volatile. They increased sharply in 2018 and the first half of 2019, making inroads into the EU27 market on the back of cheap pricing as the Brazilian real weakened and producers targeted export markets to raise hard currency. However EU27 imports from Brazil fell away sharply in 2019 as demand in the region weakened. EUTR Competent Authorities also began to increase scrutiny of imports from Brazil at this time. In 2020 and 2021, EU27 imports of Brazilian stabilised at around 120,000 tonnes on an annual basis.

Strong growth in EU27 imports of SPWPs and wood furniture

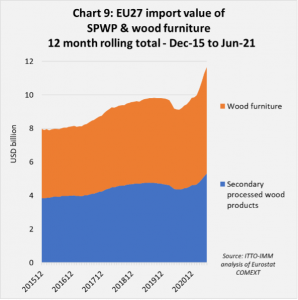

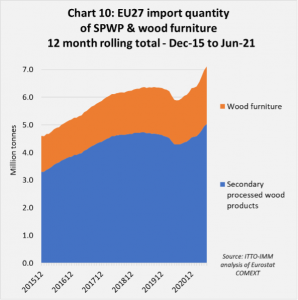

Unlike primary wood products, EU27 imports of Secondary Processed Wood Products (SPWP) and wood furniture have been rising fairly consistently in the last 5 years, a trend which is applicable to both import value (Chart 9) and import quantity (Chart 10). Rising economic and construction sector growth and consumer confidence, and the strengthening value of the euro against other currencies, led to a rapid pace of growth in 2017 and 2018. Growth slowed but was maintained in 2019 as the economy cooled. In the first half of 2020, the COVID-19 lockdowns led to a sharp but very short-lived decline in imports. Then imports rebounded strongly from the fourth quarter of 2020 and throughout the first half of 2021.

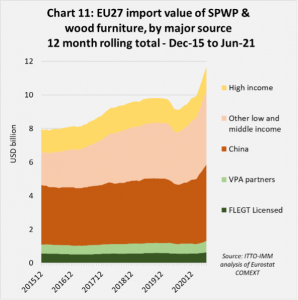

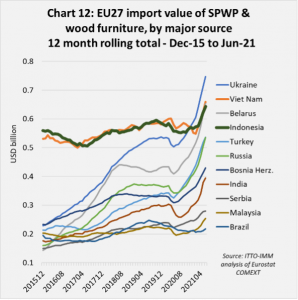

While EU27 imports of SPWPs and wood furniture from Indonesia experienced some growth after the start of licensing in November 2016, this growth coincided with a larger expansion of imports from other countries, notably China and low and middle income (LMI) countries in the European neighbourhood (Charts 11 and 12). As a result there was no gain in terms of share of total EU27 imports. In the twelve months to June 2021, FLEGT licensed timber accounted for 5.5% of all EU27 imports (by value) of SPWPs and wood furniture, down from 6.1% in the previous 12 month period and down from 6.4% in 2016 just before the start of FLEGT licensing.

Looking at imports from individual countries in more detail, the extent to which imports of SPWPs and wood furniture from Indonesia track almost exactly imports from Vietnam is very striking (Chart 12). Such a high degree of correlation in imports from a comparable country which is not yet FLEGT licensing is strongly suggestive that other economic factors unrelated to FLEGT are more important in driving trends. It follows that the more critical factors are those which Southeast Asian supply countries have in common – which might include freight, the mix of products they supply, the influence of other markets such as China and the US, and EU27 buyers’ attitudes to wood products from Southeast Asia.

The relative lack of influence of FLEGT licensing in driving market trends in the SPWP and wood furniture sector is reinforced by the much stronger growth trends since 2016 in EU27 imports from a wide range of other LMI countries entirely outside the VPA process including Ukraine, Belarus, Turkey, Russia, Bosnia Herzegovina, and India. With the exception of India, all these countries are notable for their relative proximity to the EU27, highlighting the competitive benefits of relatively shorter supply lines and turnaround times, particularly in this era of just-in-time delivery.

The more rapid pace of increase in EU27 imports from India is also significant given that Indonesian suppliers compete directly with Indian suppliers in a niche market for tropical craft-based furniture, while India has very little certified forest area and also lacks any form of legality assurance system comparable to a FLEGT licensing system. This raises questions about the forms of legality assurance being offered and accepted for EUTR conformance purposes by suppliers competing directly with Indonesian suppliers.

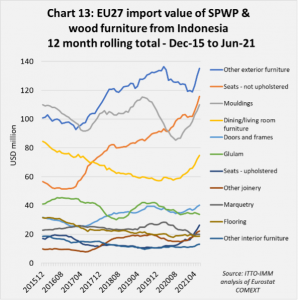

Diving into the detail of EU27 imports of SPWPs and wood furniture from Indonesia reveals that trends vary widely depending on the product group (Chart 13). At the level of individual products, at first glance, there appear to be some more positive signals from the perspective of market benefits of FLEGT licensing. Indonesia has a strong reputation in the EU27 market as a supplier of good quality wooden garden furniture, and since 2016 there has indeed been particularly strong growth in EU27 imports from Indonesia in the two product categories – “seats– not upholstered” and “other furniture” – that capture exterior wooden garden furniture. However, the assumption that this increase is driven specifically by FLEGT measures is weakened by the fact that seating, which has registered the strongest growth, is not covered by the EUTR due diligence requirement (although it is required to be FLEGT licensed).

For all other SPWPs and wood furniture types, with the possible exception of wooden doors, there has been no consistent increase in EU27 imports from Indonesia since the start of licensing in November 2016. Trade has been variable, with occasional gains typically followed by a downturn. None of this, in isolation, implies that no market benefit is to be derived from FLEGT licensing. It only shows that the benefits that may exist are obscured in trade data by other more dominant commercial factors impacting on both the supply and demand side. During 2021, the high costs of freight and high prices driven by limited supply and strong global demand have been particularly significant factors constraining Indonesia’s exports of wood products to the EU27. Indonesian suppliers have tended to prioritise exports to other markets which have recovered more quickly than the EU27 and where the competitive pressures may be less intense, notably the US.