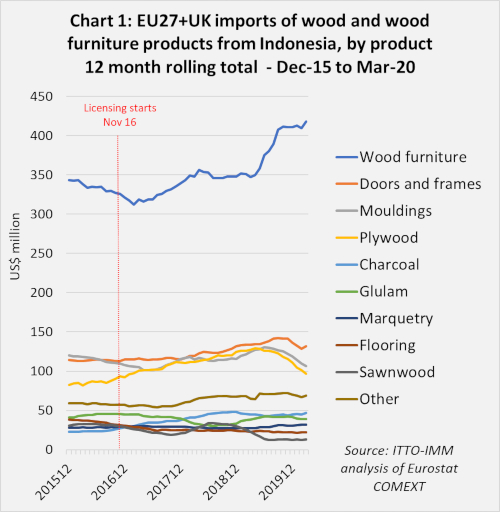

EU27+UK imports of wood furniture from Indonesia made large gains in the second and third quarter of 2019 and maintained this high level through to the end of March 2020.

In contrast to furniture, EU27+UK imports of plywood, wooden doors, and mouldings/decking from Indonesia slowed dramatically in the second half of 2019 after strong growth during the previous two years. (Chart 1).

The strong performance of Indonesian wood furniture in the European market is made more significant for occurring in the face of very strong competition, particularly from China. Embroiled in a trade dispute with the U.S. during 2019, China was looking to the EU27+UK as an alternative outlet for furniture products. EU27+UK wood furniture imports from China, by far the largest external supplier, increased 7% to US$3.74 billion in 2019, the highest level since 2010.

The pace of EU27+UK imports of plywood fell from the middle of 2019 in the face of a tightening market and highly competitive conditions, with particularly low prices for Russian birch plywood and Chinese mixed hardwood products that have been taking market share from tropical products.

There was some consolation in that direct imports of plywood from Indonesia increased in 2019 into the Netherlands (+6% to 13,000 tonnes) and Germany (+5% to 17,700 tonnes) despite the overall weakness of the market. Imports of Indonesian plywood by the Netherlands last year were double those of 2016 just before licensing started. However, the gains made in these markets in 2019 were not enough offset declining imports last year into the UK and Belgium.

Indonesian decking/mouldings was losing share in the EU market last year to products from Brazil, Peru and Bolivia. Gabon was also beginning to make inroads into this market last year.

After a strong start to 2019, European demand for Indonesian wooden doors, which is concentrated in the UK market, began to wane in the second half of the year. Indonesia is still the leading tropical supplier of other joinery products to the European market – mainly laminated window scantlings and kitchen tops – but lost some share to Malaysia in 2019 and also faces increasing competition from Viet Nam alongside a wide range of temperate suppliers in these markets.

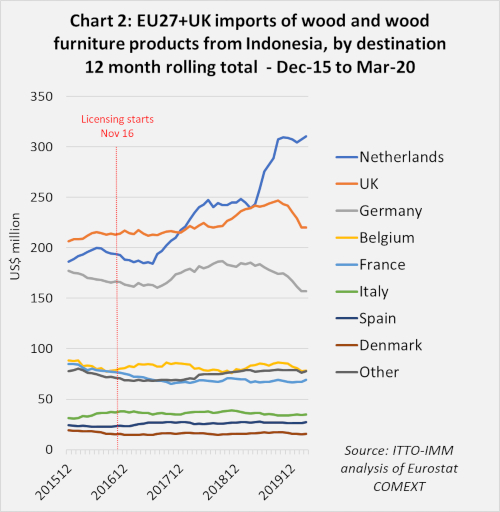

The increase in imports from Indonesia in 2019 was destined mainly for the Netherlands and, to a lesser extent, UK, Belgium and Germany (Chart 2). These are all markets where certification has been important for market development of tropical garden furniture products in the past, suggesting that FLEGT licensing was playing an important role to boost Indonesian furniture sales last year.

The Netherland’s was primarily responsible for the recent surge in imports of Indonesian wood furniture. This market remained resilient throughout 2019 and into the first quarter of 2020. Imports into the UK, Germany, and Belgium, all weakened sharply from the last quarter of 2019. Italian imports of Indonesian products were sliding throughout 2019 and the first quarter of 2020. Other EU markets remained quite stable during this period.