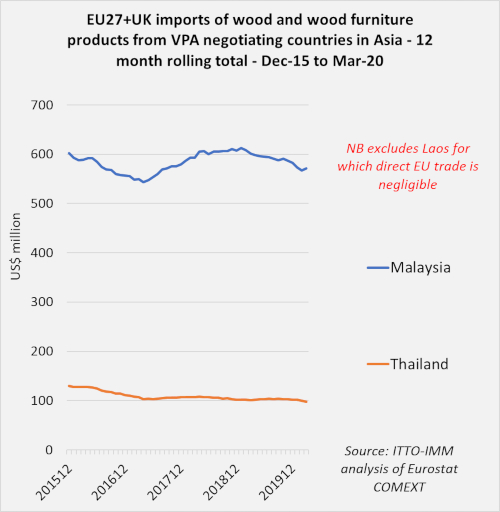

Of VPA negotiating countries, Malaysia is by far the largest supplier of tropical timber products to the EU. EU imports from Malaysia which hit a low of US$543 million in the year ending April 2017, had recovered to US$608 million in the year ending February 2019, but fell back to US$567 million in the year ending February 2020.

Despite the lockdown, EU27+UK imports from Malaysia were surprisingly strong in March this year, rising for all the main product groups, including furniture, sawnwood, mouldings and plywood.

Overall, imports of wood furniture from Malaysia strengthened in the 12 months to March 2020. Furniture imports from Malaysia mainly comprise rubberwood product for interior use at the lower end of the price spectrum, the UK being by far the largest market for these products in Europe. Significant gains were made last year in EU27+UK imports of wood bedroom furniture, wood dining-room furniture and wood non-upholstered seating.

Longer term, Malaysia has lost ground to both Cameroon and Brazil in the EU27+UK market for tropical sawn wood, and to China and Indonesia (and Russia) in the market for hardwood plywood. The decline in imports of these product groups from Malaysia in 2019 was attributed by some importers to reduced availability of PEFC certified product following the suspension of MTCS certification in Johor and Kedar states in May 2019 which led to the total certified area in Malaysia to fall by around 25%.

This may have been a factor in the Netherlands and UK where there is a stronger preference for certified wood. However, rising EU imports from other tropical countries with even less access to certified wood, such as Cameroon and Brazil, implies that other factors were also important for the decline in imports from Malaysia.

EU27+UK imports of timber products from Thailand consist primarily of furniture, with smaller quantities of plywood, fibreboard, and charcoal. The main European destinations are the UK, Germany and France. After a decline in 2016 and the first half of 2017, total EU imports from Thailand were stable at an annual level of just over US$100 million between June 2017 and January 2020. However, imports showed signs of slowing in February and March even before the main effects of the COVID long-term became apparent.