It is ironic that in 2019, just before the market chaos created by COVID-19, the EU27+UK recorded its strongest year for tropical timber product imports since 2007. That was, of course, when the last consumer boom was at its peak just prior to the market meltdown of the financial crises.

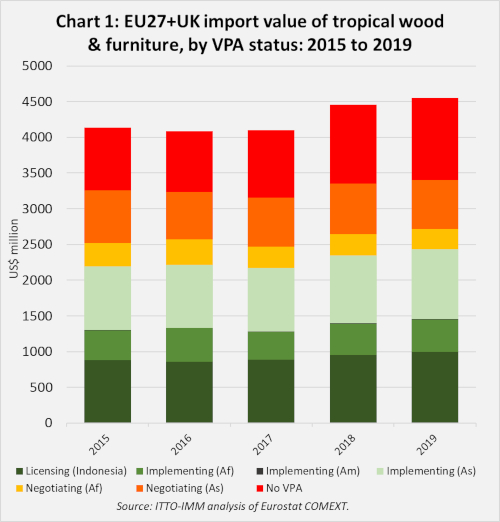

The total value of EU27+UK imports of tropical wood and wood furniture products (including direct imports and imports via third countries such as China) increased 2.2% to US$4.56 billion in 2019. This follows an 8.6% increase in import value in 2018 (Chart 1). Import quantity increased 2.1% to 2.70 million tonnes in 2019, following a 5.9% rise in 2018.

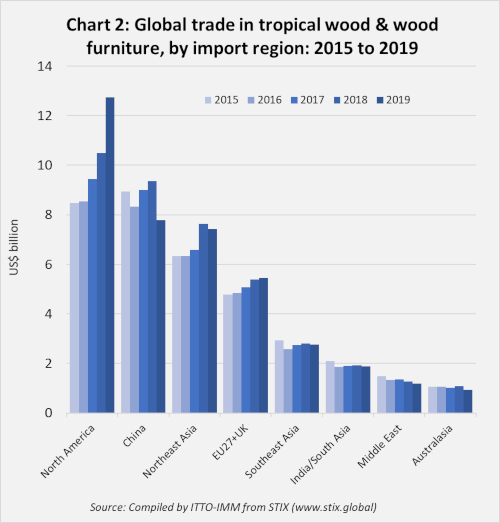

The rise in EU27+UK imports of tropical wood and wood furniture products in the last two years formed part of a wider increase in global trade. The value of global trade in wood and wood furniture products is estimated to have increased from around US$37.1 billion in 2017, to US$40.0 billion in 2018, and to US$40.1 billion in 2019.

In 2018, the rise in global trade was driven by North America (mainly US), China, and Northeast Asia (Japan and South Korea). In 2019, imports fell in China and North East Asia but accelerated into the United States (Chart 2). This was mainly due to US imports of wood furniture switching away from China in favour of South East Asian suppliers, particularly Viet Nam.

In the EU27+EU region, last year there were some positive gains for FLEGT licensed timber from Indonesia, which consolidated its position as the largest single tropical timber supply country to this market. However, the continued rise in EU27+EU imports of competing products from tropical countries with no engagement in the FLEGT process during the year raises questions about the benefits of FLEGT licensing in terms of improved overall competitiveness. Considering EU27+UK imports by VPA status (Chart 3):

- strong gains were made in the value of imports from Indonesia, the only FLEGT licensing country last year, rising 5% from US$951 million in 2018 to US$998 million in 2019. In terms of tonnage, imports from Indonesia declined 2.2% to 413,000 tonnes in 2019 following a decline of 0.3% the previous year. Taken together this implies a positive improvement in the unit value of imports from Indonesia which were focused more on furniture than lower value wood products during the year. Indonesia accounted for 21.9% of the total value of EU27+UK tropical wood-product import value in 2019, up from 21.3% the previous year.

- EU27+UK imports from the five African VPA-implementing countries – Cameroon, Central African Republic (CAR), Republic of Congo (RoC), Ghana, and Liberia – increased 3.3% to US$453 million in 2019, driven mainly by a rise in imports from Cameroon and RoC. The share of African VPA implementing countries in total EU tropical import value increased from 9.8% in 2018 to 10.0% in 2019.

- the value of EU27+UK imports from Viet Nam, the only Asian VPA implementing country, increased 3.4% to US$979 million in 2019 after rising 6.5% in 2018. Vietnam accounted for 21.5% of the total value of EU27+UK tropical wood-product imports in 2019, up from 21.2% the previous year.

- the value of EU27+UK imports from Guyana and Honduras, the two VPA countries in South America that have initialled a VPA, is negligible and fell in 2019, down 6% to US$5 million, following a 1% increase in value the year before. These countries accounted for 0.1% of the total value of EU27+UK tropical wood-product imports in both 2018 and 2019.

- EU27+UK import value from the three VPA negotiating countries in Africa declined 5.8% to US$283 million in 2019, following a rise of 1.3% in 2018. Imports from Cote d’Ivoire and Democratic Republic of Congo (DRC) were sliding during the year, while imports from Gabon were flat. These countries accounted for 6.2% of the total value of EU27+UK tropical wood-product imports in 2019, down from 6.7% the previous year.

- EU27+UK import value from the three VPA negotiating countries in Asia fell 3.6% to US$684 million in 2019. Share of these countries in the total value of EU27+UK tropical wood-product imports fell from 15.9% in 2018 to 15.0% in 2019. While imports of wood furniture from Malaysia increased, this was offset by a decline in imports of Malaysian sawnwood and plywood. Imports from Thailand were stable during the year and remained negligible from Lao PDR.

- EU27+UK imports from non-VPA tropical countries increased 4.5% to US$1.15 billion in 2019, building on a 16% gain the previous year. Share of total tropical wood product imports into the EU27+UK from non-VPA countries increased from 24.8% in 2018 to 25.3% in 2019. Most of the gains comprised wood furniture from India, sawnwood and mouldings/decking from Brazil, and tropical hardwood-faced plywood from China.

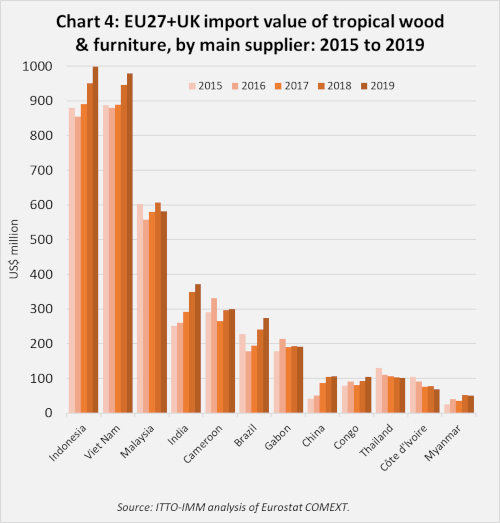

Indonesia increased its lead as the largest supplier of tropical wood and wood furniture products into the EU27+UK in 2019, staying just ahead of Viet Nam despite continued strong growth in imports from that country last year. Malaysia maintained its position as the third largest supplier to the EU27+UK last year with trade remaining broadly flat in recent years. India is consolidating its position as the fourth largest supplier having pushed Cameroon into fourth place in 2017. Imports from Brazil were rising rapidly between 2016 and 2019. Imports from Gabon have been flat. (Chart 4).

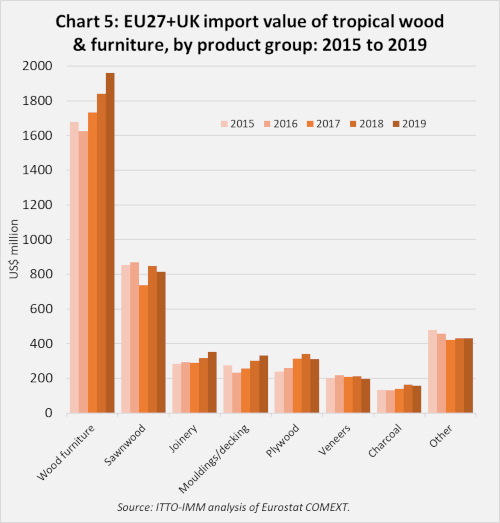

In terms of product mix, the growth in EU27+UK imports from the tropics last year was driven mainly by wood furniture (Chart 5). Import value of tropical furniture products was US$1.96 billion, up 7% compared to the previous year. The main South East Asian wood furniture supply countries – Indonesia, Viet Nam and Malaysia – have all followed a similar trajectory in the EU market in the last five years. A period of flat or declining imports between 2015 and 2018 followed by a sharp upturn in 2019.

The European market situation for tropical wood products other than furniture was more mixed in 2019. Overall, if wood furniture is excluded, there was a slight increase in the tonnage of EU27+UK imports last year, but a decrease in value. The EU27+UK imported 2.13 million tonnes of these products with a total value of US$2.59 billion, respectively 1.5% greater and 0.8% less than the previous year.

Gains made in EU27+UK non-furniture wood products imports from the tropics in the first half of 2019 were eroded in the second half as the EU economy began to slow. The first half growth was driven mainly by a recovery in imports of sawnwood from Cameroon and of sawnwood and mouldings/decking from Brazil, particularly into Belgium, together with rising imports of a variety of joinery products (doors and laminates) from Indonesia and Malaysia. These gains offset falling imports of tropical logs, charcoal, plywood, and veneers.

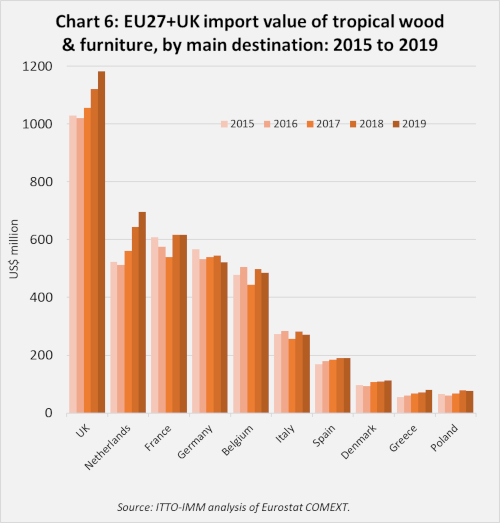

The UK remains the leading destination for tropical wood and wood furniture imports in the EU27+UK region, posting a 5% gain in 2019 to US$1.18 billion to build on a 6% increase the previous year. Imports were also rising strongly into the Netherlands, the second largest destination, up 8% last year to US$695 million after a gain of 15% the previous year. Import performance of other EU destinations was more mixed last year, remaining static in France at US$617 million after gaining 14% the previous year, while declining in Germany (-4% to US$521 million), Belgium (-3% to US$486), and Italy (-4% to US$272 million) (Chart 6).

There were gains in a few smaller EU markets for tropical wood last year including Spain (+0.3% to US$190 million), Denmark (+3% to US$113 million), Greece (+12% to US$81 million), Sweden (+2% to US$67 million), Ireland (+14% to US$63 million), Portugal (+6% to US$61 million) and Romania (+10% to US$23 million).