Assessing the current availability of third party verified products in the EU market is challenging since no system-wide data is regularly or systematically collected on the actual volume or value of trade in these products. The FSC and PEFC certification frameworks that might be expected to provide such data only publish information on the area of certified forest and the numbers of chain of custody certificates issued.

To partially overcome this obstacle, building on earlier market assessment work by other agencies starting in 2007, IMM regularly assesses the “level of exposure to third party verified/certified wood”. This is a rough measure to identify gaps in forest coverage of third party certification and other legality verification procedures. It is based on the percentage area of certified or legally verified commercial forest area in each individual supplier country. For example, if 40% of a country’s forest area is known to be independently certified or legally verified, the level of exposure of wood production and exports in that country is assumed to be 40%. The certified/verified forest areas are calculated by comparing data from the various certification and verification systems with UN FAO figures for areas of productive forest land.

‘Level of exposure’ data can be broken down by verification system, including FSC, PEFC and FLEGT licensing. For the IMM assessment, wood from countries covered by FSC-endorsed Controlled Wood National Risk Assessment (CWNRA) is also considered ‘third party verified’. To avoid double counting, areas dual certified to FSC and PEFC are accounted separately.

Overall the results suggest that the drive to promote responsible timber procurement practices in EU trade is having an effect, both to increase the area of forest verified as low risk of illegal harvest in major supply countries, and to encourage an overall shift in trade towards countries with greater access to verified products.

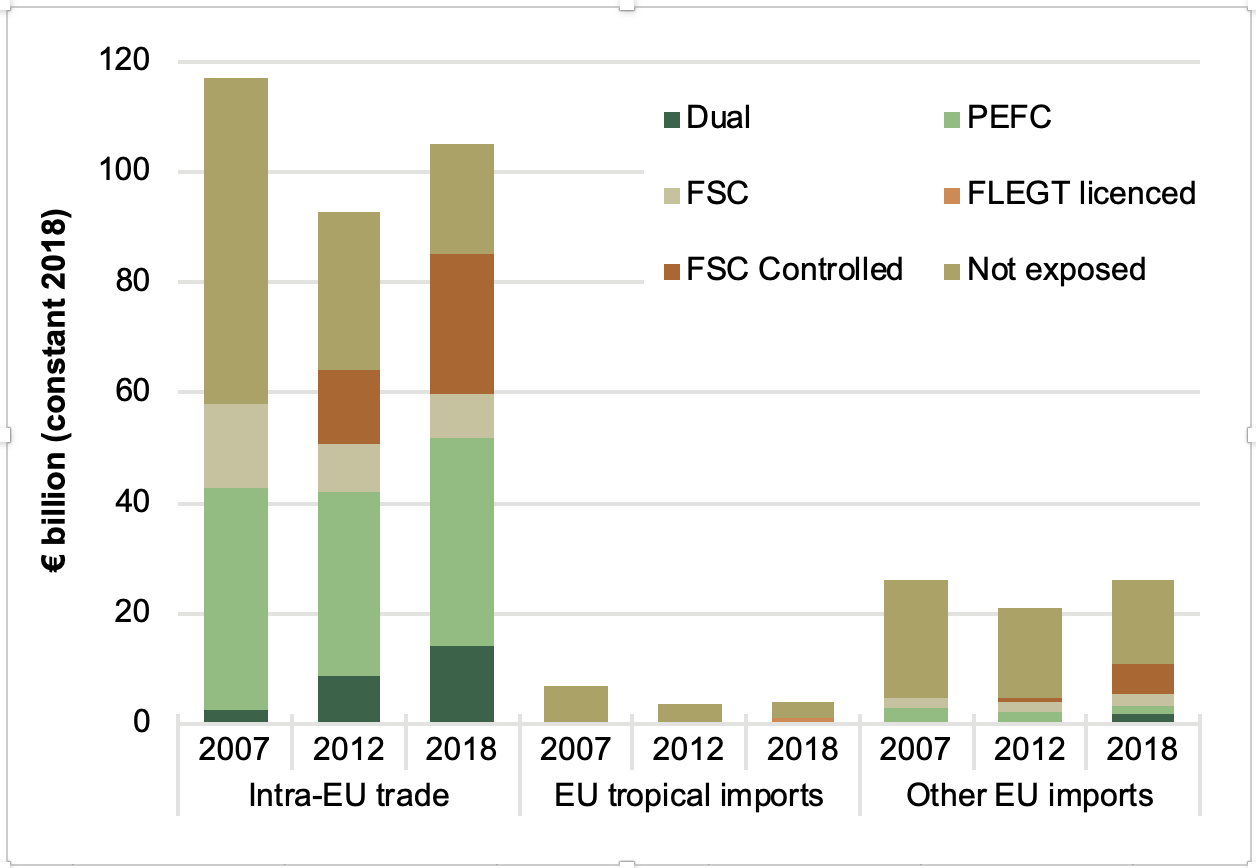

In 2018, 81% of internal EU trade in all EUTR regulated timber and timber products was “exposed” to some recognised form of third party verification. This compares to 69% in 2012 and 50% in 2007. This reflects the very large and growing proportion of forest area in the EU that is either certified or assessed to be low risk of illegal harvest by an FSC CWNRA.

Figure 1: Exposure to verification in EU trade of EUTR regulated products, by verification system and main source region

Source: IMM analysis of Eurostat Comext, FAO Forest Resource Assessment, FSC and PEFC data

Exposure to third party verification of all EU timber products imports from non-tropical regions outside the EU was 42% in 2018, compared to 23% in 2012 and only 18% in 2007. This is partly due to a rise in both the proportion of forest verified and the share of EU imports from countries in Eastern Europe, notably Russia, Belarus, Ukraine, Serbia, Bosnia, and Turkey. There has also been a slight increase in certified forest area in China, the largest external timber supplier to the EU, over this period. However, a more significant factor driving the rise in exposure is the publication of FSC CWNRAs indicating low risk of illegal harvest in Canada, USA, Norway, and Switzerland, all of which are large suppliers of timber products to the EU.

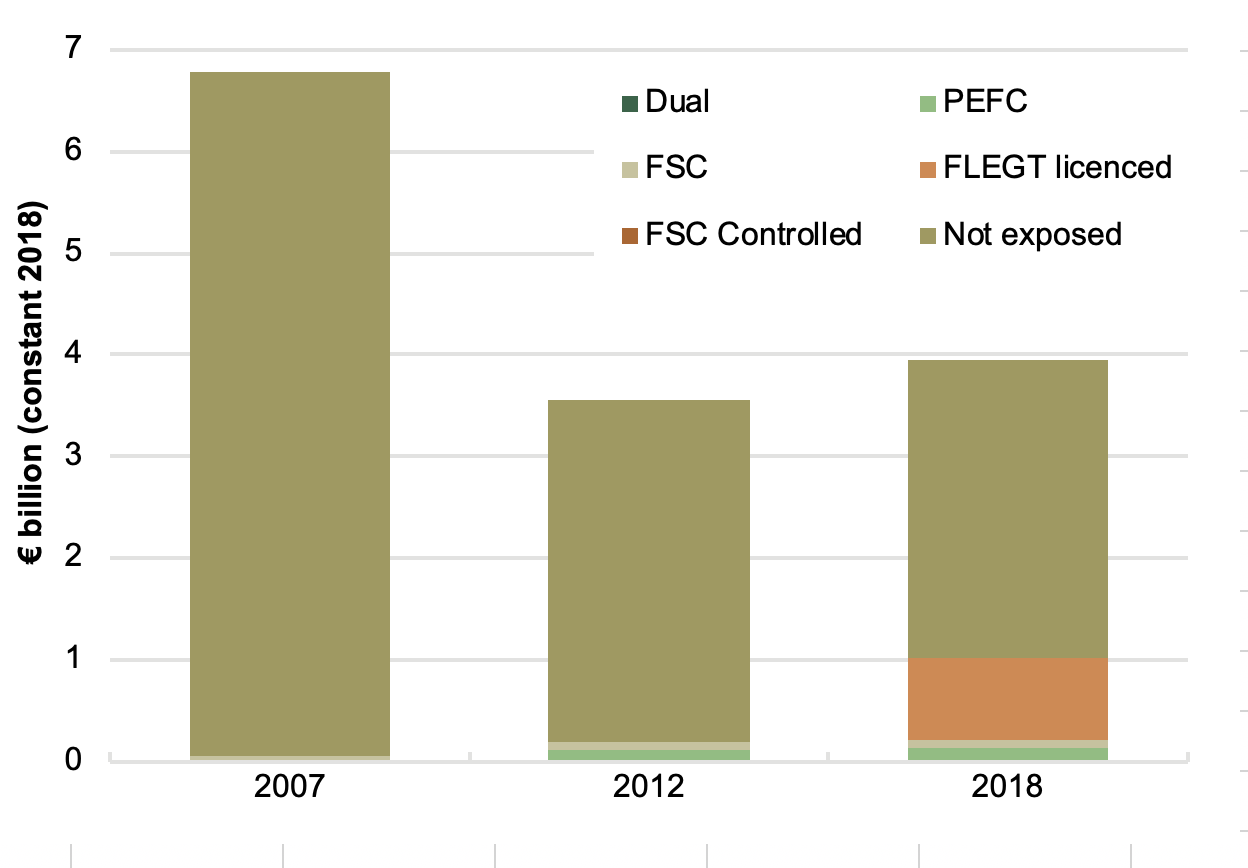

Exposure to third party verification of all tropical timber imports was 25.8% in 2018, up from 5% in 2012 and less than 1% in 2007. All the gain between 2012 and 2018 was due to FLEGT licensing of Indonesian product which accounted for 20.5% of all EU imports of tropical timber. Exposure to FSC and PEFC certification in total EU imports of tropical timber and timber products was 5.3% in 2018, a slight increase from 5.2% in 2012. The lack of increase is indicative of the slow pace of uptake of certification in tropical countries.

The assessment indicates that if all timber from the 9 countries that in 2018 were either licensing, or were implementing or had initialled a VPA, the level of exposure to verified product in EU tropical trade would have been 49.4%. If all 15 VPA partner countries were included, the level of exposure would have been 67.7%.

Figure 2: Exposure to verification in EUTR regulated tropical timber imports, by verification system

Source: IMM analysis of Eurostat Comext, FAO Forest Resource Assessment, FSC and PEFC data

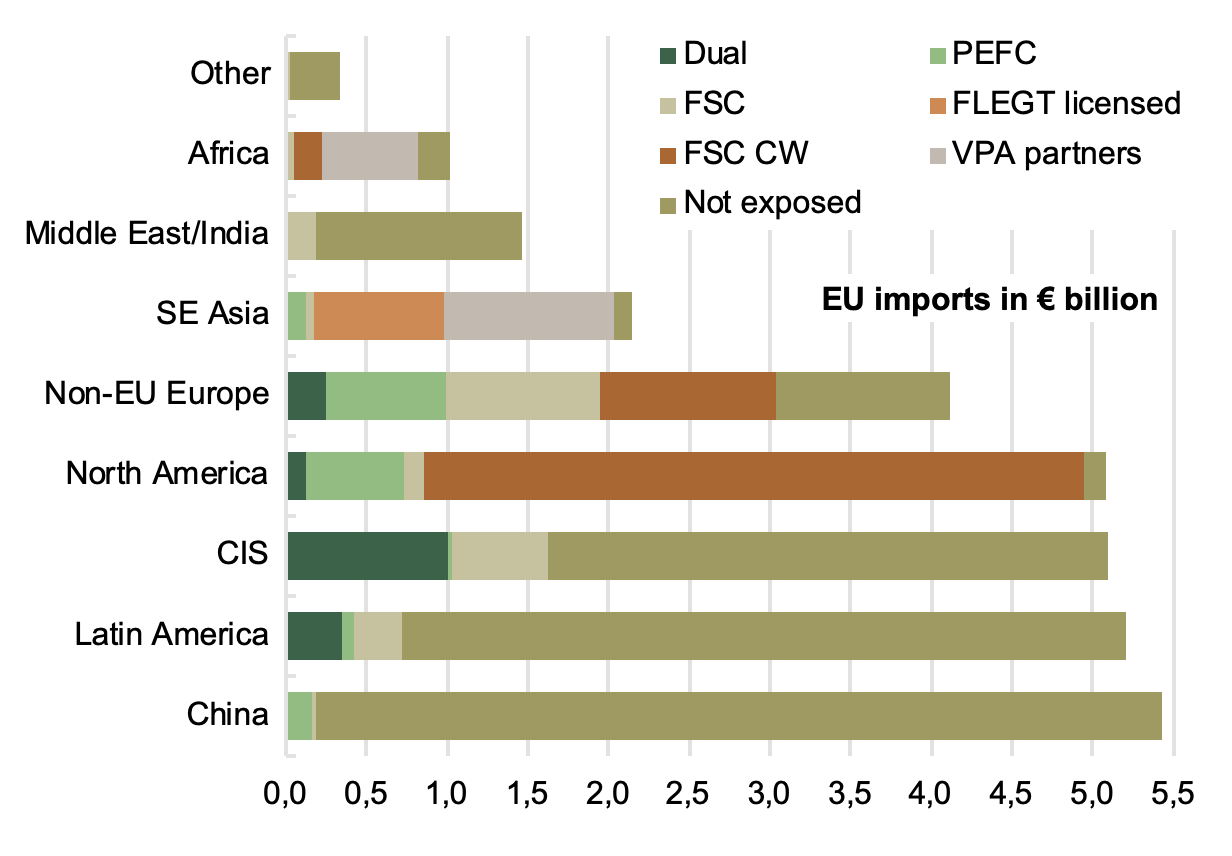

While the level of exposure has increased, in 2018 a large proportion of EU imports were still not exposed to verified sources or engaged in the VPA process. Figure 11.5.3 shows that China dominates amongst EU-supplying countries with low exposure to verified timber. China’s level of exposure to certification is expected to increase in the future, but the rate of change is uncertain. The China Forest Certification System (CFCS), endorsed by PEFC in February 2014, had certified only 6.6 million hectares of China’s over 200 million hectares of forest by the end of 2018. An additional 1 million hectares in China were certified by FSC. Much of the certified forest area is natural protection forest and China’s large area of production plantation forest is still largely uncertified.

Figure 3: Exposure to verification in EUTR regulated timber imports, by region of supply and verification system, 2018.

Source: IMM analysis of Eurostat Comext, FAO Forest Resource Assessment, FSC and PEFC data

Latin America is assessed to have relatively low level of exposure to certification and verification. However, this figure is severely distorted by reliance on forest area to calculate the index. The Amazonian rain forest is, of course, huge and only a tiny proportion is certified. But this area only contributes a relatively small volume of timber to international trade. Most of the wood product imported into the EU from Brazil now constitutes softwood or eucalyptus from plantations outside the tropical zone (including large quantities of chemical pulp), much of which is certified. Therefore, the index underestimates the real level of exposure of Latin American wood products in EU trade.

A similar situation prevails in Russia where the certified area, at over 50 million hectares in 2018, is enormous but still represents only 6% of Russia’s total forest area (of over 800 million hectares). The certified area in Russia is concentrated mainly in the western part of the country where trade is oriented more towards the EU.

The Middle East (mainly Turkey) and India, where there is only very limited exposure to verification, have emerged as more important suppliers of timber products to the EU in recent years.

While the VPA process captures only a relatively small proportion of total EU imports of timber and timber products, it is very significant amongst tropical supplying countries in South East Asia and Africa. If all timber products imported by the EU from VPA countries were FLEGT licensed, the level of exposure to verified timber from South East Asia would rise from 46% to 95% and from Africa from 22% to 80%.