After a dip in 2017 and the early months of 2018, EU imports of tropical wood products recovered ground in the second half of 2018 and gained momentum in the first five months of 2019. EU imports from Indonesia have increased in value terms but remain stubbornly flat in tonnage terms. There was significant recovery in EU imports of sawnwood from Cameroon in the year to May 2019. Most other gains during this period were in imports from countries not engaged in the VPA process, including Brazil, China, India, Panama, and Cuba.

EU imports of tropical hardwood faced plywood continued to rise from China, much of it destined for the UK. However, the biggest single increase in recent months has been in imports of sawn wood from Brazil. A significant proportion of the gain in import volume from non-VPA countries comprised products outside the scope of the EU Timber Regulation, particularly for energy production.

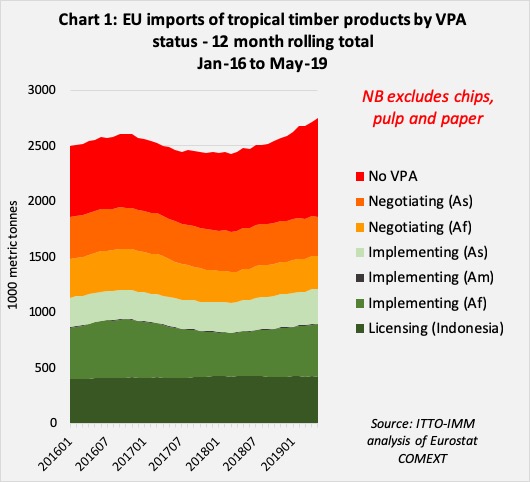

The EU imported 2.75 million metric tonnes (MT) of tropical timber products (excluding chips, pulp and paper) in the year ending May 2019, up 11% from 2.47 million MT in the previous 12-month period (Chart 1).

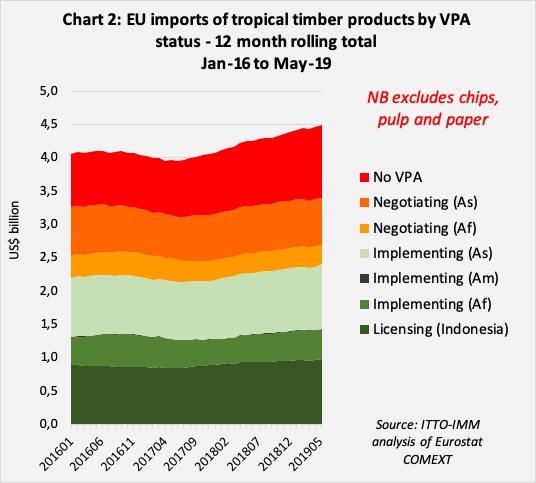

Over the same timespan the dollar value of EU tropical timber imports increased 6% from $4.25 billion to $4.50 billion (Chart 2).

As the dollar strengthened against the euro during this period, there was a larger 10% increase in the euro value of EU tropical timber imports, from €3.57 billion to €3.94 billion.

Imports from Indonesia up 5% in value but flat in tonnage terms

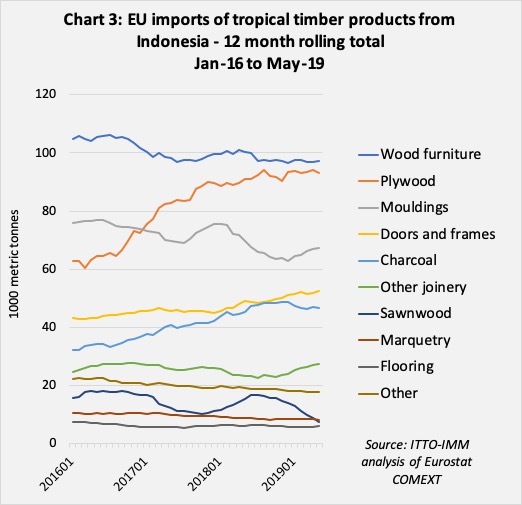

EU imports from Indonesia, currently the only FLEGT licensing country, decreased slightly (-1%) in tonnage terms in the year to May 2019. EU imports from Indonesia were 423,000 MT during this period, compared to 428,000 MT in the previous twelve months. In value terms, imports increased 5% from US$932 million to US$976 million.

The pace of growth in EU imports of Indonesian plywood and charcoal has slowed, while imports of S4S sawnwood has declined after rising in 2018. More positively EU imports of doors and other joinery products have increased from Indonesia. EU imports of wood furniture from Indonesia have remained flat. Imports of Indonesian mouldings/decking have been volatile on a monthly basis, but the total in the year to May 2019 was similar to the previous 12-month period (Chart 3).

Imports from Africa recovering lost ground

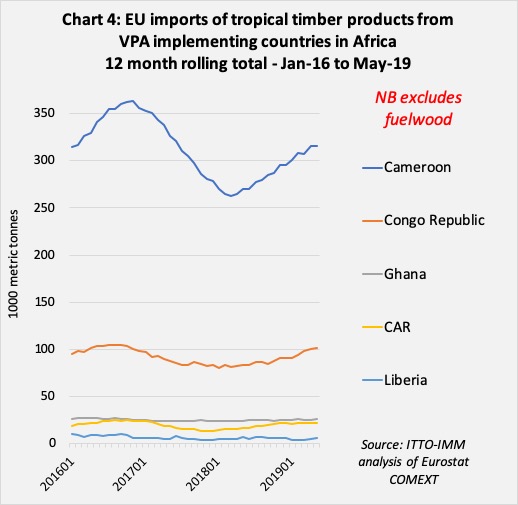

EU imports from the five VPA implementing countries in Africa (Cameroon, Central African Republic, Congo Republic, Ghana, and Liberia) have been very volatile in recent years. 12-month rolling imports increased sharply to 524,000 MT in September 2016 and then fell even more rapidly to a low of 385,000 MT in March 2018. In the following months, imports recovered much of the lost ground to reach 470,000 MT in the year ending May 2019, 17% more than in the previous 12-month period.

Most of the recent volatility in EU trade in timber from African VPA implementing countries is attributable to sawnwood imports from Cameroon, particularly in Belgium. EU trade with Cameroon rebounded strongly in the twelve months to May 2019. There were also gains in imports of sawnwood from Congo Republic and of logs and sawnwood from Central African Republic during this period (Chart 4).

EU imports from Ghana, mostly of sawnwood, have remained low and flat for the last four years, with the 12-month rolling total stable at 25,000 MT. EU imports from Liberia have also hardly changed during this period, averaging around 5,000 MT per year.

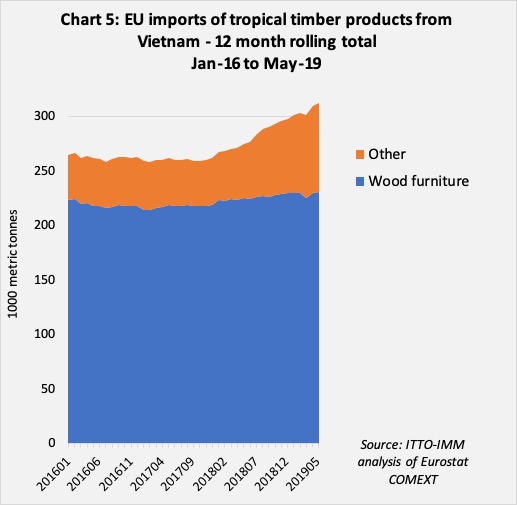

Rising imports from Vietnam

Vietnam completed VPA negotiations in 2018 and is moving on to the VPA implementation phase this year. 12-month rolling total timber product imports into the EU from Vietnam were 313,000 MT in the year ending May 2019, 14% more than the previous 12-month period. While EU imports from Vietnam continue to be dominated by wood furniture (HS 94), much recent growth has been in imports of a range of other wood products in HS 44, notably charcoal and other energy wood, plywood, laminated wood, planed sawnwood, and doors (Chart 5).

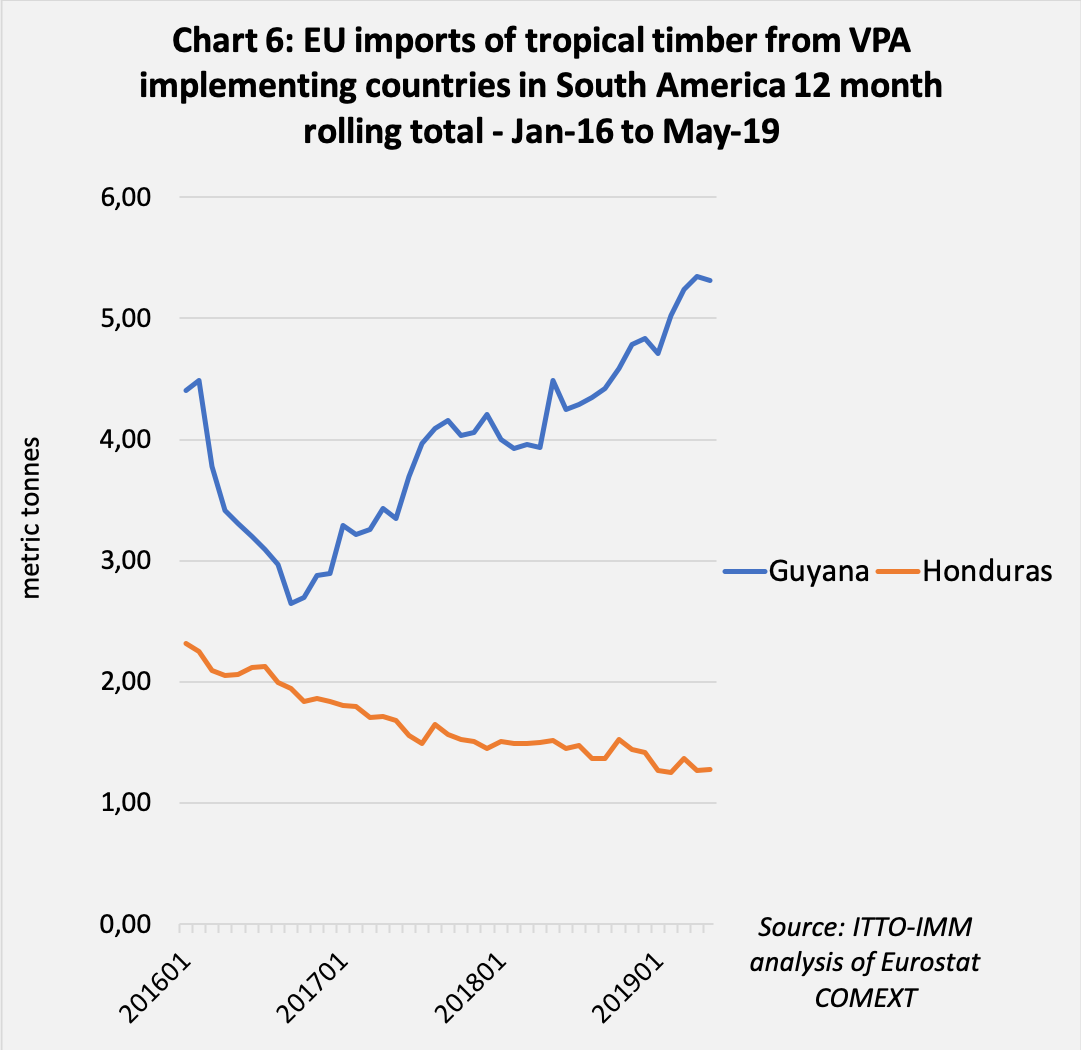

The two countries in Latin America that recently completed VPA negotiations, Guyana and Honduras, are currently only small suppliers of timber to the EU.

EU imports from Guyana, mainly consisting of hardwood logs and sawn, tend to be quite volatile with demand strongly focused on a specialist niche market for heavy duty sea and river defence applications. EU imports fell sharply from 8,000 MT in 2015 to only 3,000 MT in 2016, but have recovered ground since then, rising to 5,300 MT in the year to May 2019, 18% more than in the previous 12-month period.

Imports into the EU from Honduras, mainly sawn softwood, have been falling in recent years. 12-month rolling total imports from Honduras were 1,280 MT in the year to May 2019, 16% less than in the previous 12-month period (Chart 6).

Changing product mix from Malaysia

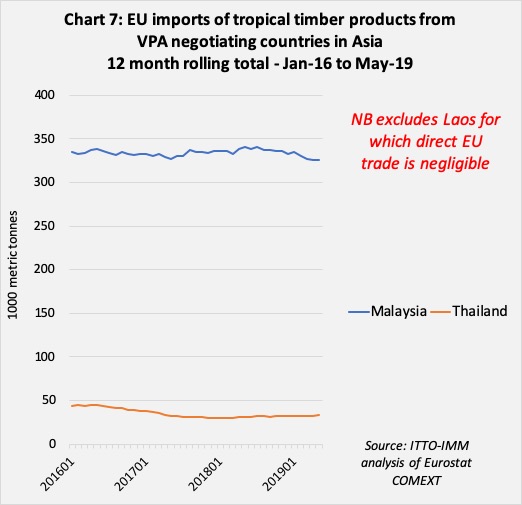

Of VPA negotiating countries, Malaysia is by far the largest supplier of tropical timber products to the EU. EU imports from Malaysia totalled 326,000 MT in year to May 2019, 5% less than in the previous 12-month period. In recent months, Malaysia has lost ground to both Cameroon and Brazil in the EU market for tropical sawn wood, and to China and Indonesia (and Russia) in the market for hardwood plywood. However, EU imports of wood furniture from Malaysia have continued to strengthen, while there has also been some recovery of EU imports of window scantlings and other joinery products from Malaysia.

EU imports of timber products from Thailand consist primarily of furniture, with smaller quantities of plywood, fibreboard, and charcoal. Total EU imports from Thailand were 33,000 MT in the year to May 2019, 7% more than in the previous 12-month period (Chart 7).

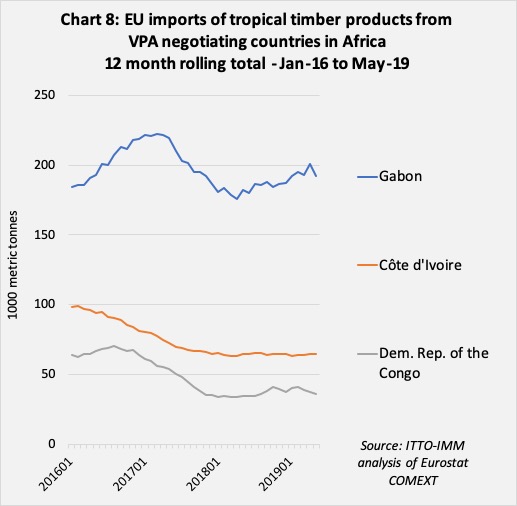

Of the three VPA negotiating countries in Africa, Gabon is the largest supplier to the EU (Chart 8).

After declining in 2016 and 2017, and flatlining in 2018, EU imports from Gabon have recovered ground in 2019. In the year to May 2019, imports from Gabon were 192,000 MT, 5% more than the previous 12-month period. Much of the recent growth has comprised sawnwood and veneer. Imports of plywood and sleepers from Gabon have weakened.

After declining sharply in 2016 and 2017, EU imports from Côte d’Ivoire have stabilised at a lower level. Imports of 65,000 MT in the year to May 2019 were exactly equivalent to the previous 12-month period. EU imports from Côte d’Ivoire are now split roughly half and half between sawnwood and veneers. A continuing decline in EU sawnwood imports from Côte d’Ivoire is being compensated by a rise in veneer imports.

After a sharp decline in 2017, there was a short-lived upturn in EU imports from DRC in the last quarter of 2018, the effects of which were already waning by May 2019. Imports of 36,000 MT in the year to May 2019 were only 5% more than in the previous 12-month period. Most of the recent gains were in log and veneer imports from DRC, while imports of sawnwood from this country continued to decline.

Large and sometimes rising imports from non-VPA countries

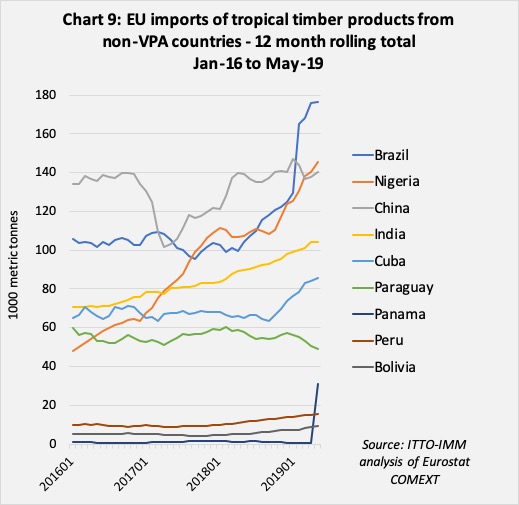

EU imports of tropical timber products from countries not engaged in the VPA process increased 24% from 713,000 MT in the year to May 2018 to 885,000 MT in the year to May 2019. This is primarily due to a recovery in imports of hardwood sawnwood and decking from Brazil and a continuing rise in tropical hardwood plywood imports from China and of furniture from India. EU imports of mouldings/decking also increased significantly from Peru (+48% to 11,900 MT) and Bolivia (+86% to 7,200 MT) in the year to 2019.

The rising trend in EU imports of tropical wood from non-VPA countries has been intensified by a significant increase in imports of products for the biomass sector. There was a sudden large increase in imports of wood pellets from Panama in May 2019 which may or may not be the start of a longer-term trend. Also, a large increase in imports of hardwood logs from Brazil which, on closer analysis, can be identified as plantation grown eucalyptus likely destined for pulp or biomass.

Recent gains in charcoal imports from Cuba and Venezuela have offset a decline in imports of this product from Paraguay. Meanwhile imports of charcoal from Nigeria have continued at a relatively high level (Chart 9).