Like all manufacturing and construction materials and products, timber has to meet customer and specifier criteria on price, quality, performance and availability. But arguably more than most competing materials, it also has increasingly to satisfy procurement policy requirements on proof of legality and sustainability.

This was the premise of Workshop 2 at the Barcelona Consultation; “Recognising priorities and purchase dynamics for tropical wood: Assessing how supply chain relationships develop and the relevance or impact of FLEGT licenses”.

Speakers and delegates addressed customer criteria on sustainability and legality, acceptable forms of proof (including the relative trust placed in certification and FLEGT licensing) and to what extent these factors were actually considered important purchasing considerations in the marketplace.

George White opened discussions by summarising studies on private and public sector timber procurement he has led for IMM.

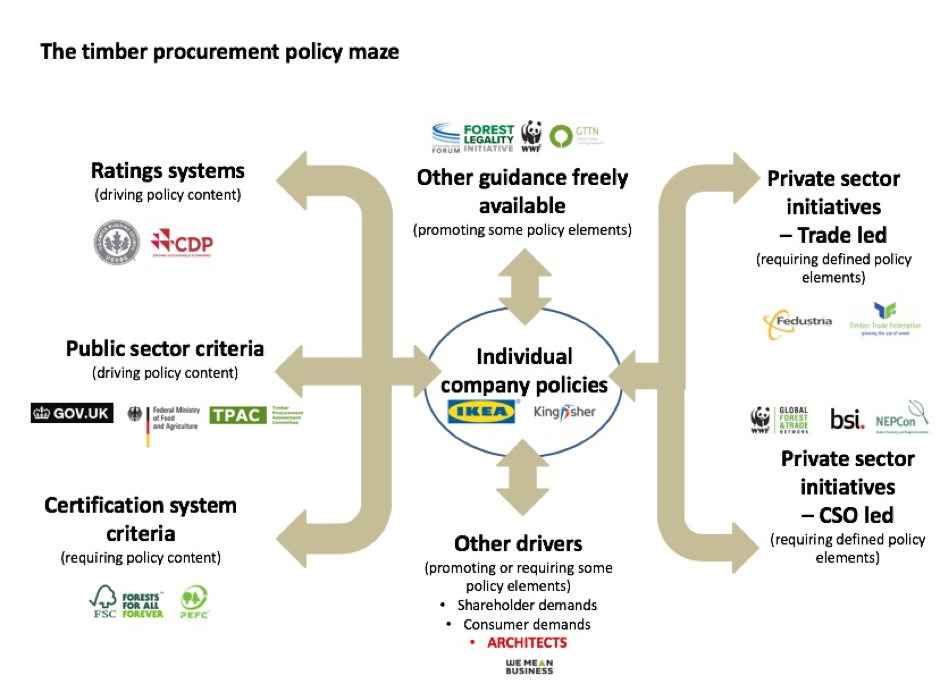

The private sector study looked at the significance of 65 potential influences on procurement policy. Of 20 major EU timber buyers covered, 19 had a defined procurement policy. Sixteen incorporated certification as a requirement and 13 legality verification, but only two mentioned FLEGT. The conclusion was that there is ‘still a long way to go’ for FLEGT to become established as an EU private sector procurement requirement.

The timber procurement policy maze

The public procurement study showed 22 EU member states currently operating specific timber procurement policies. They all accept certification as proof of legality and sustainability (albeit applying different definitions of these terms). Of these, 18 recognise FLEGT licensing in some capacity, but only the UK and Luxembourg on a level with FSC and PEFC certification. Others accept licensed goods only where certified are not available, or as proof of legality only.

Moreover, the study reported that only two EU countries operated mandatory local government timber procurement policy. As local authorities account for 70% of all government procurement, that left ‘considerable room for non-compliance’.

From these findings, the conclusion was that currently ‘EU government procurement was not a remedy to drive [market acceptance] of FLEGT licensing’. It also seemed unlikely to become so without a ‘push for more mandatory procurement policy’.

George white

Architects as market influencers

The next IMM study, now underway, is looking at the role of the EU’s 500,000 architects as timber market influencers and the factors shaping their materials specification. It is assessing the importance of their role in construction supply chain decision making, their wider knowledge and perception of wood generally and tropical timber in particular, their information sources, the importance they attach to proof of sustainability and their awareness and perceptions of FLEGT.

The study is also evaluating the influence of green building schemes in timber use and their acknowledgement of FLEGT. From their experience, delegates said architects had a poor environmental image of tropical timber, little knowledge of its technical performance and would have limited if any awareness of FLEGT. “Some have simply rejected tropical timber’s use, largely on environmental grounds,” said one.

The consensus was that the profession was worth targeting, but required focused communication.

Customer requirements

Delegates were also asked to share their views on other factors shaping the timber business and customer purchasing decisions, and particularly the role sustainability and legality play in the latter. They represented a broad spectrum of the industry, with product areas including sawn tropical hardwoods, hardwood generally, decking, plywood, constructional timber, engineered wood products, flooring, joinery, and veneers. Sources of supply were also wide ranging, including Brazil, the US, China, other European countries and Africa – notably Cameroon. Customer sectors ranged from merchant/wholesalers and joinery manufacturers, to shopfitters, carpenters, and hospitality fit-out specialists.

Broader market concerns included Spanish and wider European political and economic uncertainty and Brexit and its potential impact on Spanish tourism. On the wider international stage, US-China and US-EU trade tensions were adding to economic anxiety, as was slowdown in the Chinese economy.

Other market factors mentioned included the price suppressing impacts of online retail, reinforced by the market-shaping strategies of big timber product and retail brands – the so-called ‘Ikea effect’. An ongoing decline in traditional woodworking skills in the EU was also said to be driving imports of more finished timber products.

Considering factors shaping customer purchasing decisions

On the part played by sustainability and legality verification in the marketplace, the consensus was that the most common definition of the former was FSC or PEFC certification. At the same time, some delegates said that still few people further down the supply chain, other than those involved in public or blue-chip private projects, had sustainability requirements. One participant estimated it was mentioned by just 5% of his customers. Some customers were willing to pay a premium for certified timber, generally where they needed it to secure a contract or to meet the requirements of green building schemes.

No delegates reported customers asking for or inquiring about FLEGT-licensed wood products. This was thought to be partly because only Indonesia was issuing FLEGT licences and it was not a major supplier to Spain. “If Cameroon was licensing, there might be more awareness,” said one participant. But others said the ‘natural assumption’ that wood was legal also limited wider FLEGT interest. It also meant that they could not charge a premium for licensed goods.

Some felt communicating the wider social and environmental impacts of the FLEGT VPA process might help raise its profile. However, one delegate questioned whether the average wood consumer was interested in this aspect of the supply chain story, any more than the ‘average person buying a t-shirt from Zara’.

Indonesian FLEGT systems firmly embedded

Puri Listiyani, Director of Indonesian Trade Promotion Centre, Barcelona, told the Consultation that FLEGT systems in the country were today firmly established and that licence processing was ‘easy, fast and efficient’.

A total of 23 million ha of forest and 4,200 timber producers had been FLEGT audited, and between 2013 and 2018 Indonesia had exported $54 billion of timber and wood products certified under its SVLK timber legality assurance system – the TLAS underpinning FLEGT. Since 2016, when Indonesia started licensing, its exports had included 80,000 FLEGT-licensed shipments.

Puri Listiyani