The IMM 2017 annual report has looked into both the relative international competitiveness of all VPA partner countries based on their rating by several international competitiveness indices and in more detail into the perception of VPA implementing partners’ competitiveness by the European import trade.

Several VPA partner countries, especially Malaysia, Indonesia, Viet Nam and Thailand, ranked highly in one or more of the international competitiveness indices analysed by IMM, namely the World Bank’s “Ease of Doing Business” (EDB), the World Economic Forum Global Competitiveness (GC) Index, and the UNCTAD Liner Shipping Connectivity Index:

- Malaysia remained by far the top performer amongst VPA Partner countries across the indices. In spite of the recent fall in the connectivity Index, it remains among the world’s five most connected countries. However, Malaysia continued to fall slightly – from rank 23 to 24 (2013: 6) – on the EDB index. Compared to other VPA partner countries this is still a very good rating though. On the GC Index Malaysia also lost ground – from 18th to 25th position in 2017

- Indonesia’s position on the GC Index remained stable at 41st in 2017. At the same time, ranking on the EDB Index continued to increase sharply from 120th in 2013 to 91st in 2016 and 72th in the 2017/2018 report. The country made significant progress on a number of items including “starting a business”, “access to electricity”, “paying taxes”, “trading across borders”, “protecting minority interests”, “access to credit” and “registering property”. Indonesia’s connectivity remains a problem, being considerably lower than key competitors including China, Malaysia, Viet Nam and Thailand. However, while the connectivity rating for Malaysia, Thailand and Viet Nam has trended slightly down recently, Indonesia’s rating has improved during 2015-2017 and the gap between it and Viet Nam and, in particular, Thailand has narrowed. Malaysia and China remain far better connected though.

- Between 2013 and 2016, Thailand fell from 18th to 46th on the EDB index, due to range of issues including “construction permits”, “registering property”, “paying taxes”, “trading across borders” and “enforcing contracts”. However, most of the lost ground was regained in 2017/2018, when Thailand rose to 26th rank. At the same time, Thailand’s Connectivity Index declined slightly from 2016-2017 and on the GC if fell from 32nd to 34th rank.

- Viet Nam’s ranking on the GC index increased from 70th in 2013 to 60th in 2016 and 2017. Viet Nam’s EDB index ranking increased from 99th in 2013 to 82nd in 2016 and again to 68th in 2017/2018 as the country made ground on several issues including “access to electricity”, “access to credit”, “trading across borders” and “enforcing contracts”. Viet Nam’s connectivity Index softened slightly in 2017 after a sharp improvement in 2016.

- Lao PDR’s overall performance is weak compared to other Asian VPA partner countries. The country’s ranking on the GC index fell from 81st in 2013 to 93rd in both 2016 and 2017. Ranking on the EDB increased from 159th in 2013 to 139th in 2016 before falling again to 141st in the most recent report. Lao is not listed on the connectivity Index.

- Ghana slipped sharply down the EDB index from 67th in 2013 to 108th in 2016 and then further to 120th in 2017/2018. In 2016 ranking was down significantly on several issues including “dealing with construction permits”, “access to electricity”, “registering property”, “access to credit”, “protecting minority investors”, “paying taxes”, “trading across borders”, “enforcing contracts” and “resolving insolvency”. In 2017, the country apparently only made progress on the issue of “construction permits”. Ranking on the GC index was stable at a low level (114th) between 2013 and 2017. On the connectivity Index Ghana fell behind Gabon in 2017 and remained slightly lower than Congo and Côte d’Ivoire.

- Côte d’Ivoire’s competitiveness is still low but showing some signs of improvement. The country’s ranking on the GC index increased from 126th in 2013 to 99th in 2017. During the same period, ranking on the EDB index increased from 167th to 142nd in 2016 and then again to 139th in 2017/2018.

- Congo’s connectivity Index increased between 2013 and 2017 to a significantly higher level than that of Ghana and Côte d’Ivoire; however, it remains very low by international standards. There was also a slight improvement in Congo’s ranking on the EDB index from 185th in 2013 to 179th in 2017/2018.

- Liberia’s ranking on the EDB fell from 144th in 2013 to 174th in 2016 with a significant decline across a wide range of issues including “Dealing with construction permits”, “Access to electricity”, “Access to credit”, “Paying taxes”, “Protecting minority investors”, and “Trading across borders”. It improved again slightly to 172th in 2017/2018. Liberia’s Connectivity Index remains very low also compared to the other African VPA partner countries. On the GC it fell from rank 129 to 131 between 2015 and 2017.

- Cameroon slipped from 114th to 119th rank in the GC Index between 2015 and 2017. The 2017/2018 EBD report listed some improvements in “starting a business” and “access to credit” last year but Cameroon still only held 163th place in the EBD ranking. Cameroon’s Connectivity Index improved slowly over the last few years and is now relatively close to Ghana’s or Côte d’Ivoire’s but still clearly lower than Congo’s.

- There was little or no change in the very low level of competitiveness and connectivity exhibited by other VPA partner countries in Africa including Central African Republic, DRC and Gabon.

- Between 2013 and 2016, Honduras’s ranking on the GC index increased from 111th to 88th, where it remained in 2017. Its ranking on the EDB increased from 127th to 105th between 2013 and 2016 and then fell back again to 115th. Honduras’ connectivity Index has recently improved a little but is still at a low level, comparable to that of Ghana or Côte d’Ivoire.

- Guyana’s ranking on the GC index fell from 117th in 2014 to 121st in 2015; it was not listed among the 138 countries in the 2017 report. Ranking on the EDB fell from 115th in 2013 to 124th in 2016 and 126th in 2017/2018. Guyana’s points on the connectivity Index doubled in 2017, but the country’s connectivity still remains lower than that of Honduras, Ghana or Côte d’Ivoire.

EU trade perception: Indonesia playing in a different league than African VPA implementing countries

As a part of the IMM 2017 European trade survey respondents were quizzed about their own experience with VPA implementing partner country competitiveness. The questions included an inquiry into perceived overall competitiveness of each country as well as competitiveness against a range of indicators including:

- Price

- Availability/Lead time/Logistics

- Technical performance

- Legality assurance

- Assurance of sustainability

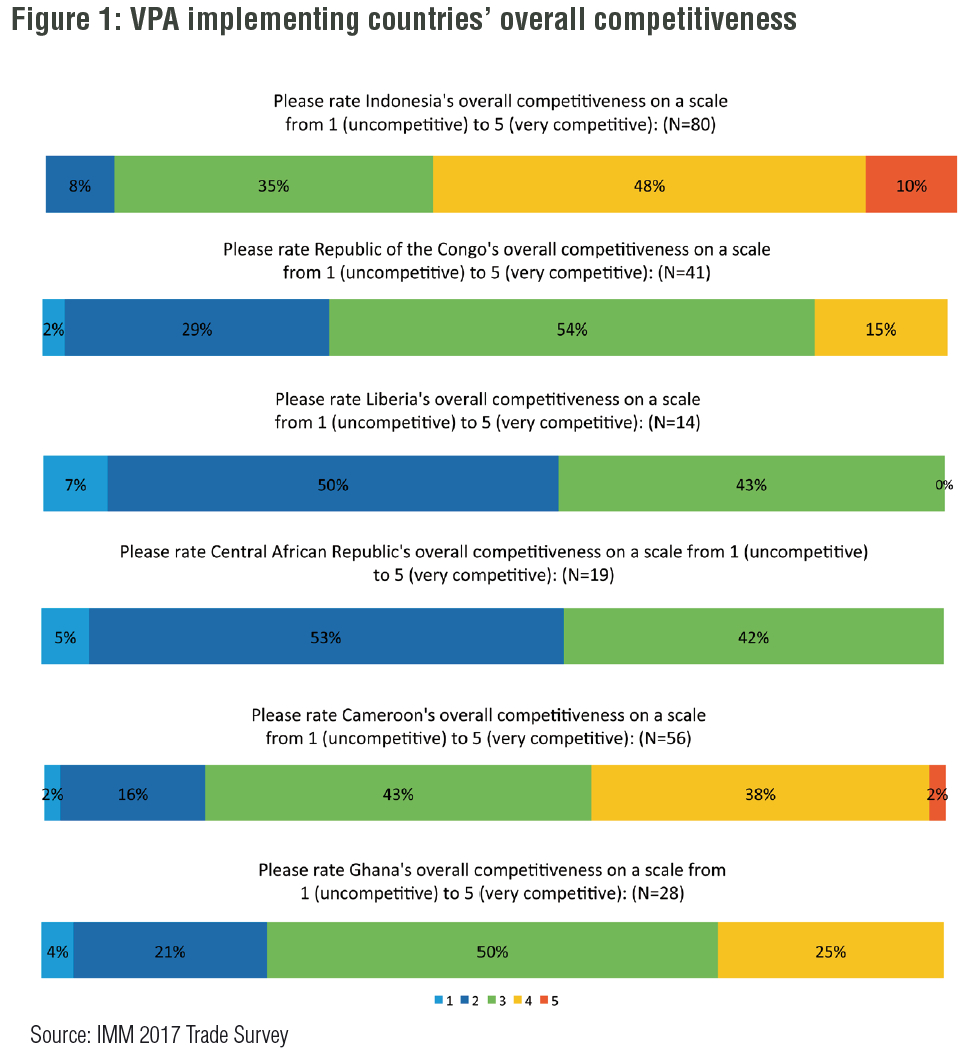

As in the international indices, Indonesia was ranked the most competitive by far among the FLEGT-licensing and VPA-implementing countries also by the European trade. A number of respondents remarked it was “playing in a different league” than the African VPA implementing countries.

90% of respondents rated Indonesia’s overall competitiveness very good to satisfactory; 58% rated Indonesia’s competitiveness “good” or “very good”.

The African VPA partner countries achieved satisfactory and good ratings primarily in the areas of “product range” and “technical performance”; while supplying primarily sawn timber and some logs to the EU markets, the African VPA countries deliver several commercial wood species that can be found nowhere else in the world.

Among the African partner countries, Cameroon was the only one to be ranked “very competitive” overall by a small number of respondents (2%). The country also achieved the best average rating of all African implementing countries, with only 18% of respondents ranking it “uncompetitive” or “very uncompetitive”.

Ghana and Congo Republic were ranked “uncompetitive” or “very uncompetitive” by 26% and 31% of respondents, respectively, and around 50% gave a “satisfactory” rating in each case. Both countries also had a number of “good” ratings.

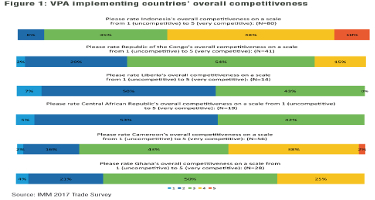

Liberia and Central African Republic performed weakest among the African VPA implementing partner countries. 57% and 58%, respectively, of the European survey respondents ranked the two countries “uncompetitive” or “very uncompetitive” overall. No respondent rated Liberia and CAR “competitive” or “very competitive” overall.

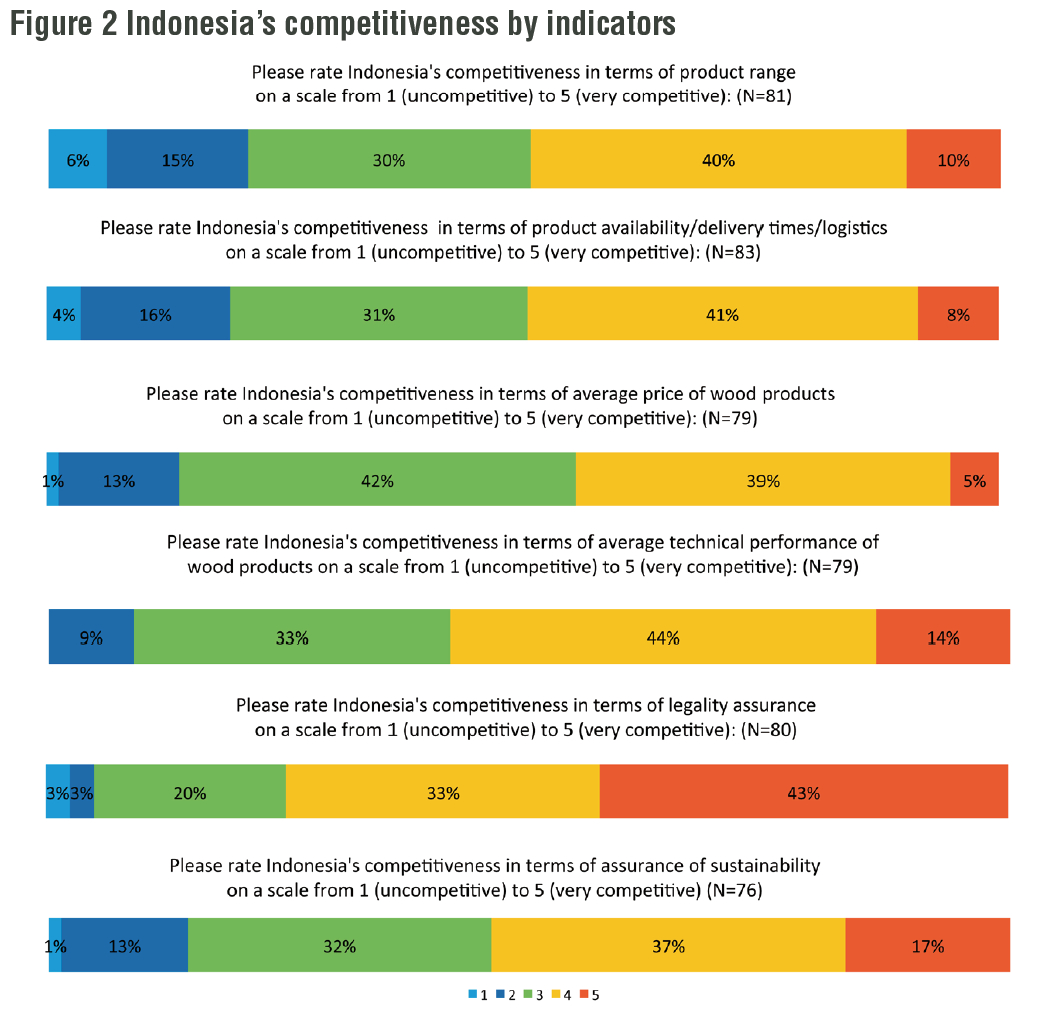

Indonesia performs particularly well in “legality assurance”, “technical performance” and “assurance of sustainability”

A closer look at the different indicators of price, availability/logistics, technical performance, legality assurance and assurance of sustainability (Figure 2) shows that Indonesia performed particularly well in “legality assurance” (76% “competitive” or “very competitive”), “technical performance” (58% “competitive” or “very competitive”’) and “assurance of sustainability” (54% “competitive” or “very competitive”).

The competitiveness rating for the “product range” may have been affected by a reportedly comparatively low level of commitment of some suppliers in the furniture sector to keep up with European product trends and fashion. One or two furniture importers remarked they were scaling back imports from Indonesia for this reason. IMM will look into the separate indicator of “adapting to (European) fashion trends” in the follow-up competitiveness ranking planned for 2019. At that time, more Asian partner countries will also be included in the follow-up ranking to enable comparison of Indonesia against its direct competitors.

Anecdotal evidence gathered during the first IMM Trade Consultations in spring 2018 indicate that Indonesia performs well in terms of “quality/technical performance” as well as “reliability/protection of intellectual property” against Asian competitors. However, Viet Nam and China, in particular, were often said to be one step ahead when it comes to “price”, “mass production”, and “adapting to trends”. Moreover, China, Malaysia, and Viet Nam were all reportedly performing better than Indonesia when it comes to “logistics”.

A baseline analysis of the Indonesian furniture sector’s competitiveness relative to other Asian and European suppliers can be found in the IMM EU Furniture Sector Scoping study.

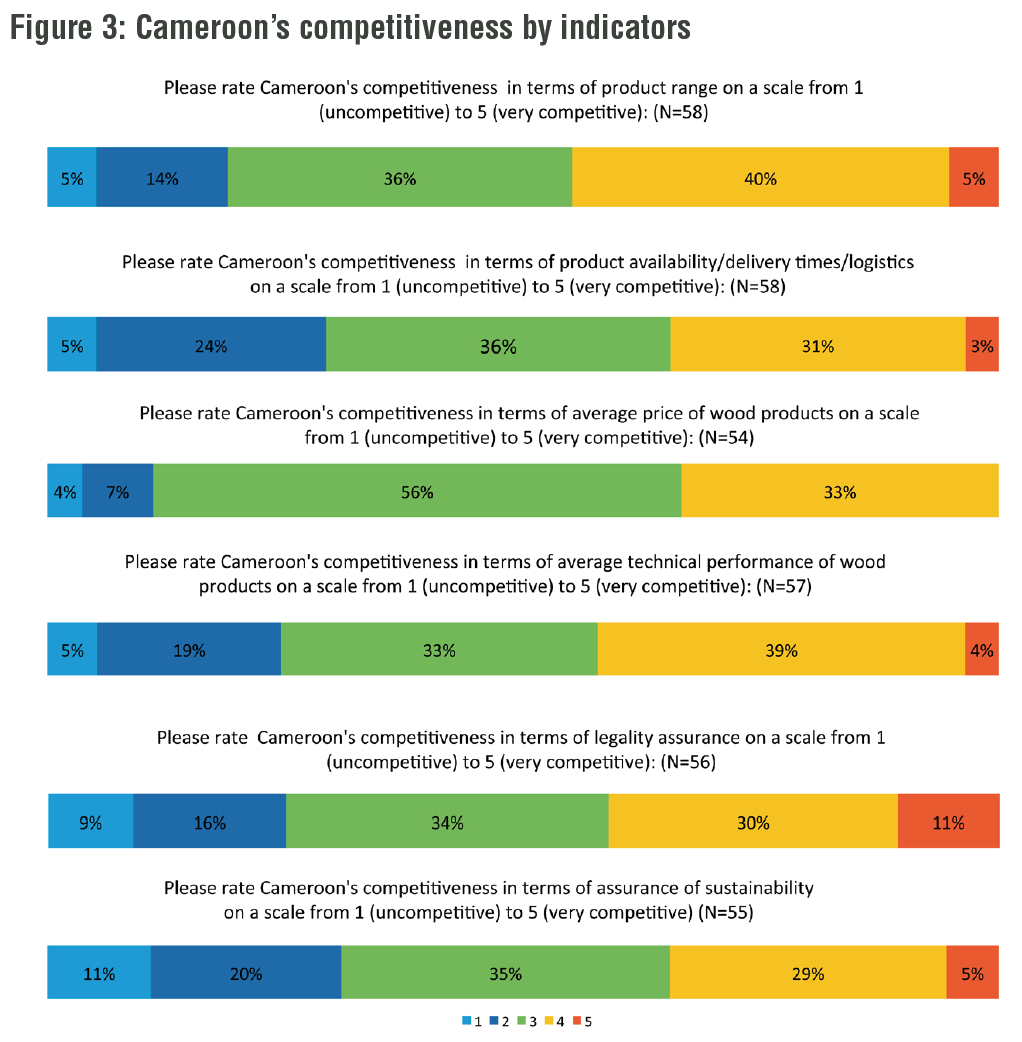

European trade appreciates broad range of timber species supplied by Cameroon

Figure 3 shows that Cameroon achieved comparatively good ratings in terms of “product range” (45% “competitive” or “very competitive”) and “technical performance” (43% “competitive” or “very competitive”).

The country exports mainly sawn timber to the EU. It offers a broad range of popular species including Sapelli, Ayous, Azobé, Iroko, Okan and Tali, among others, and is the single most important supplier of tropical sawn timber to a number of the key EU markets. Cameroon performed better than all the other African VPA implementing countries against practically all indicators and was the only African VPA partner country to receive a small number of “very competitive” votes across all indicators.

Against the background of Cameroon’s importance as a tropical timber supplier and the relative political stability in the country, numerous European survey respondents called for a speedy completion of VPA implementation in the country.

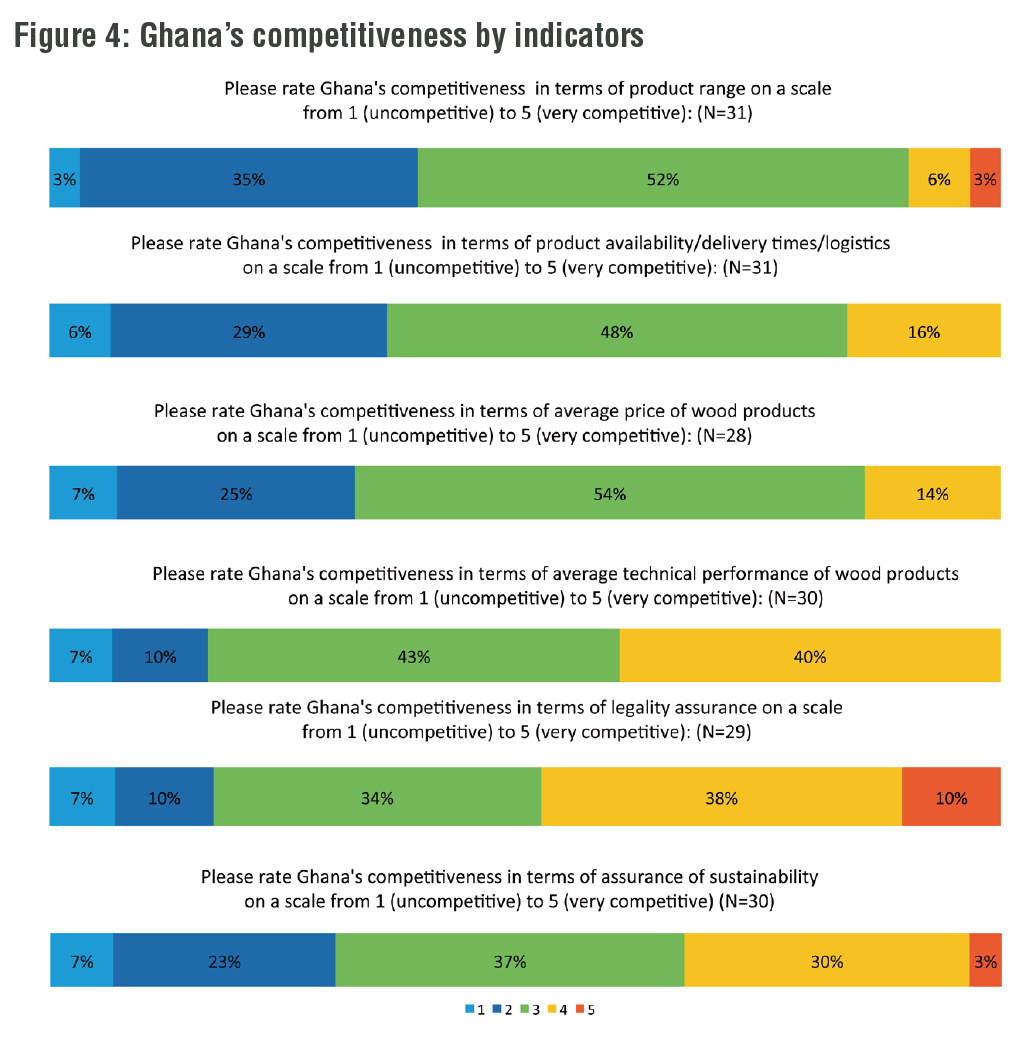

Ghana performed relatively strongly in “assurance of legality”

Analysis of the different indicators shows that Ghana performed relatively strongly in “assurance of legality” (48% “competitive” or “very competitive”). Here, the country has likely profited from the advanced state of VPA implementation and the related awareness of major exporters of the EUTR (Figure 4).

Ghana also performed relatively well in terms of “technical performance” – 40% of respondents gave a good rating here – and “assurance of sustainability” (33% “competitive” or “very competitive”).

The mainly satisfactory to low ratings in terms of “product range” and “availability/lead times” are not surprising given the loss of importance of Ghana as a tropical timber supplier for the EU market over the last decade.

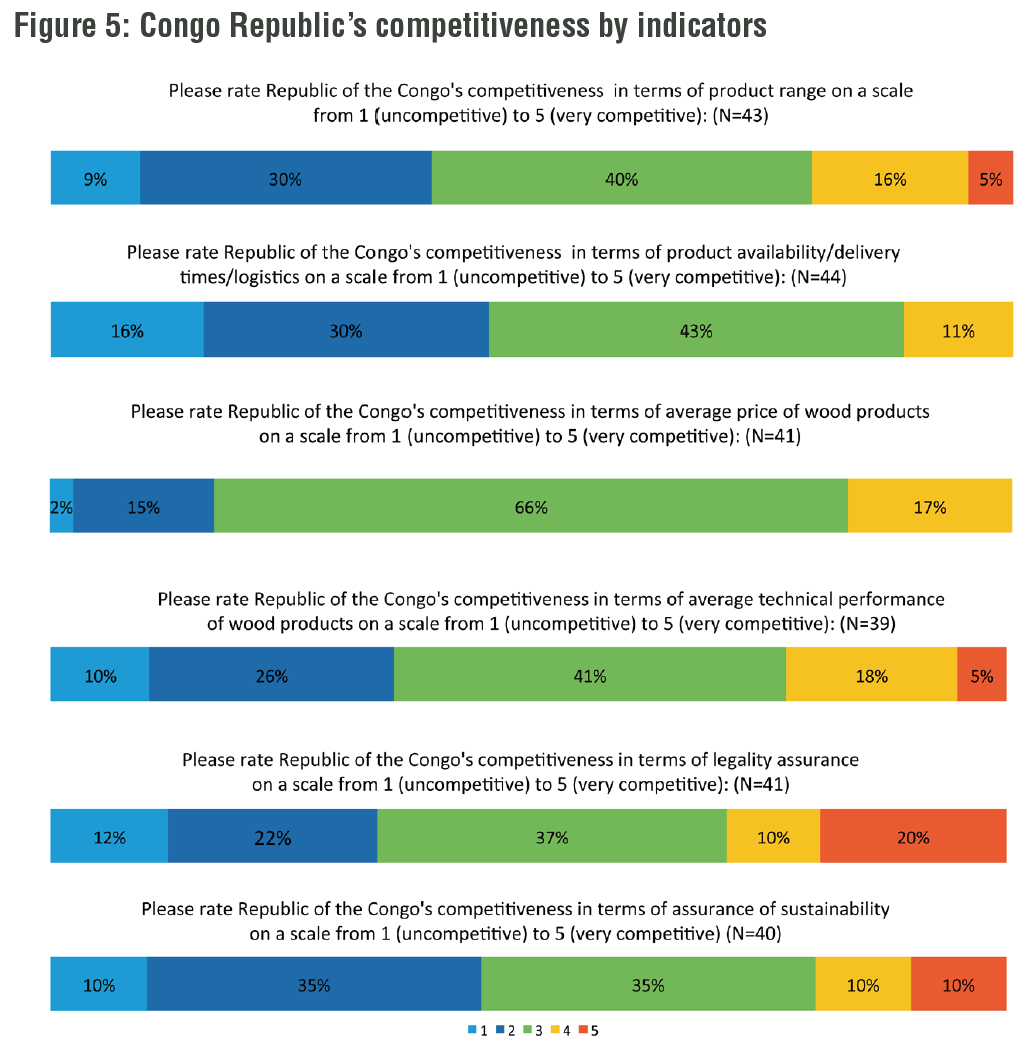

ROC shows relative strength in “price”, “product range” and “technical performance”

RoC’s ratings were lower on average than those of Cameroon and Ghana, but the country still had quite a significant proportion of average to very good ratings especially in terms of “price”, “product range” and “technical performance” (Figure 5).

Like all other African VPA partner countries Congo Republic supplies primarily sawn timber to the EU markets. Within the EU, Congo Republic is an important supplier primarily for Belgium and France.

For assurance of legality (and sustainability) buyers reportedly mostly rely on FSC certification in the Congo.

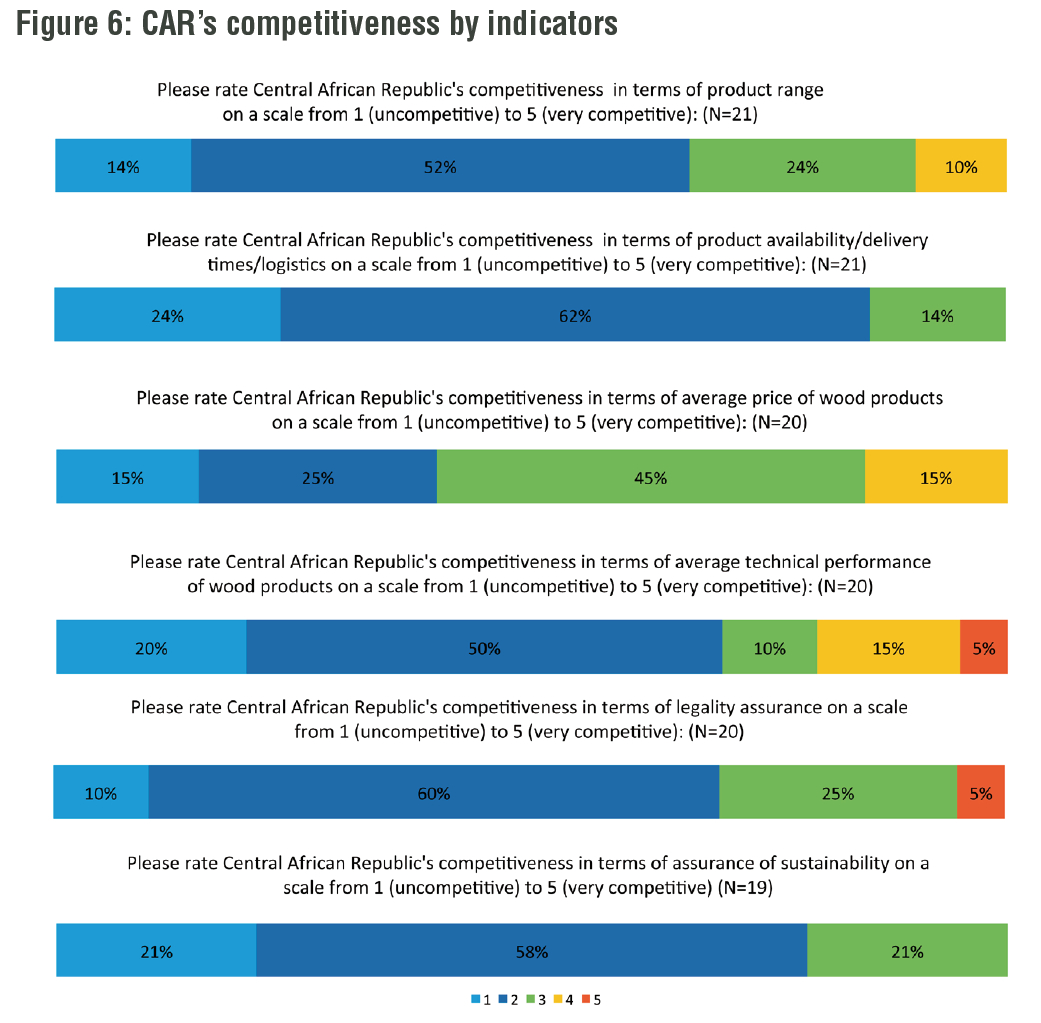

“Price” identified as strongest feature in CAR and Liberia’s competitiveness ranking

The Central African Republic was rated relatively competitive in terms of “price” by a number of survey respondents. In most other categories, around two-thirds of respondent rated the country “uncompetitive” or “very uncompetitive” (Figure 6).

According to comments from the IMM trade survey, the civil war and its aftermath has made sourcing wood in CAR difficult – especially of verified legal timber.

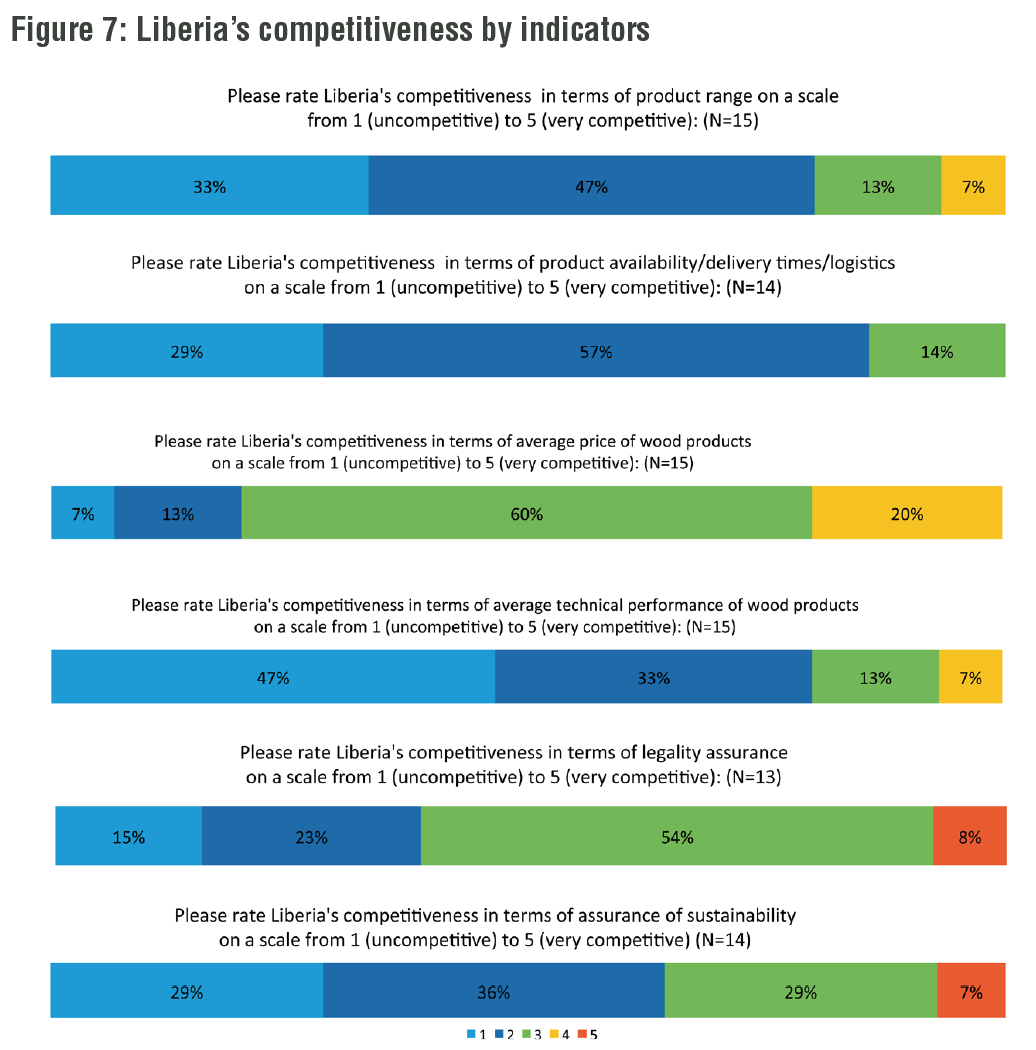

Like for CAR, Liberia’s main strength was identified in the area of pricing by the competitiveness ranking (Figure 7).

Surprisingly, given that obtaining legality assurance in Liberia was frequently described as particularly difficult during interviews with IMM correspondents, is the comparatively good rating for “obtaining proof of legality”. One reason for this may be that only a relatively small number of survey respondents participated in the competitiveness ranking for Liberia (13-15 companies, depending on the indicator. By way of comparison, Indonesia was ranked by around 80 and Cameroon by 50-60 companies).

The small number of respondents engaged in Liberia may have specialised in sourcing from there and thus be used to carrying out risk assessment and mitigation in the country. Liberia’s rating against the other indicators was weak.