FLEGT-licensed timber in the EU market

Full report, French Executive Summary, Bahasa Executive Summary

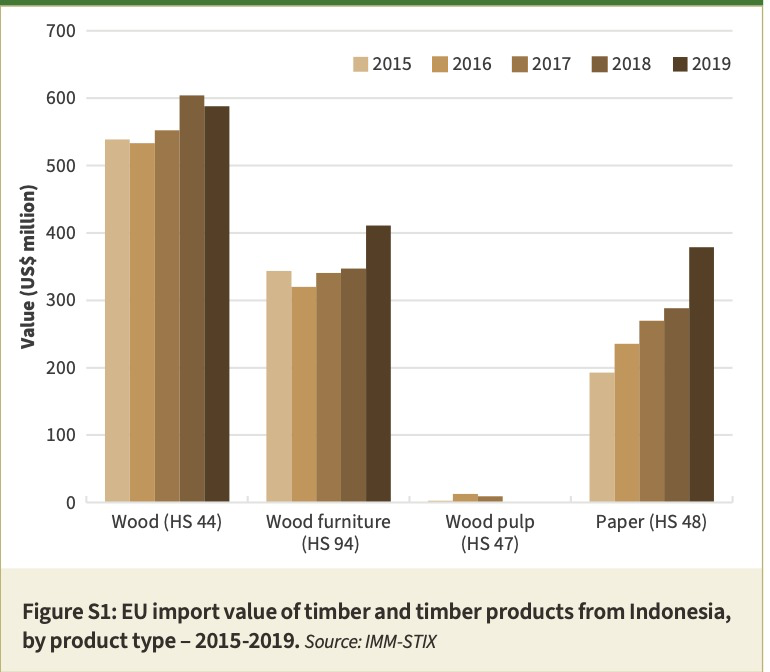

This latest IMM Annual Report, “FLEGT VPA Partners in EU Timber Trade 2019” shows EU import value of timber and timber products1 from Indonesia, the only FLEGT licensing country, increased 11% from US$1.24 billion in 2018 to US$1.38 billion in 2019. This followed a 6% gain between 2017 and 2018. In quantity terms, EU imports from Indonesia increased 14% from 676,000 tonnes in 2018 to 769,000 tonnes in 2019, after falling 6% in 2018.

EU import growth from Indonesia in 2019 was dominated by wood furniture, which rose 18% to US$411 million, and paper products, which also increased sharply, by 31% to US$379 million. On the other hand, the value of EU imports of wood (HS 44) products from Indonesia decreased 3% from US$604 million in 2018 to US$588 million in 2019 losing some of the 9% gain made in 2018. Imports of wood pulp from Indonesia, always limited, were close to zero in both 2018 and 2019 (Figure S1).

The rise in EU imports of FLEGT-licensed wood products from Indonesia coincides with a wider recovery in EU demand for wood products generally. Activity in key EU wood end-use sectors, such as construction and furniture, bottomed out in 2013 and then recovered at a slow, but relatively consistent rate until 2019. China, Russia and other countries in the Commonwealth of Independent States (CIS) region remained the dominant partners in EU import trade, although some tropical countries, particularly Indonesia, but also including Viet Nam, India and Brazil, began to make new inroads in the EU market, most notably in the furniture sector.

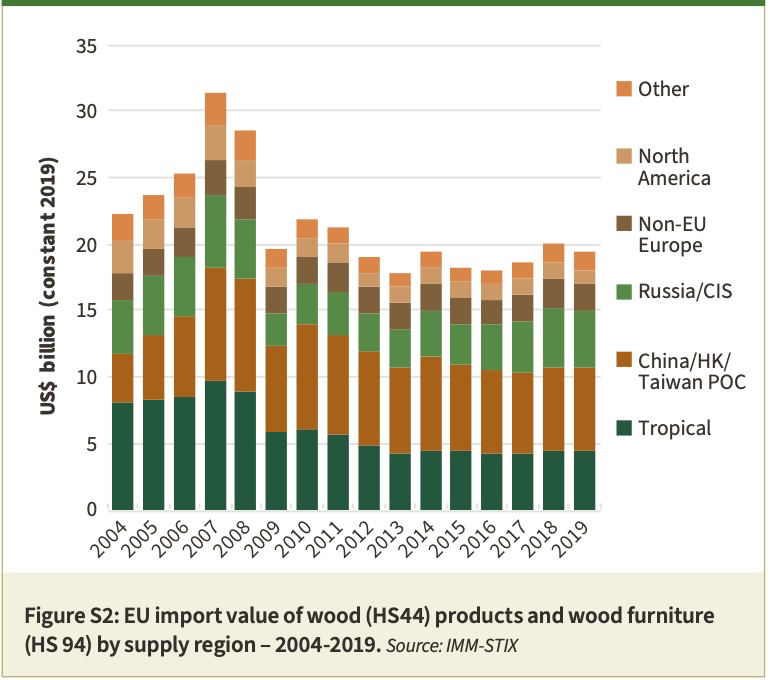

The total value of EU imports of wood products was US$19.3 billion in 2019, 3% less than the previous year (Figure S2).

However due to weakening of the euro against the dollar, there was a 3% increase in euro import value, to €17.3 billion. Import value in 2019, reported in euro terms, was the highest level since 2008. Import quantity declined 2.5% to 26.0 million tonnes in 2019.

In 2019, China maintained its position as the largest external supplier of wood products to the EU. The total value of wood product imports from China (excluding those identified as composed of tropical hardwoods) increased 3% from US$6.12 billion in 2018 to US$6.29 billion in 2019, mainly due to a partial recovery in imports of Chinese furniture and to a lesser extent joinery products and plywood. By contrast, after several years of rapid growth, EU imports of wood products from CIS countries fell 7% from US$4.56 billion in 2018 to US$4.25 billion in 2019. The share of CIS countries in total EU imports declined from 23.3% in 2018 to 22.0% in 2019. EU imports of wood products from North America declined 11% from US$1.15 billion in 2018 to US$1.02 billion in 2019. The region’s share of total EU imports of wood products fell from 5.9% to 5.3% during this period.

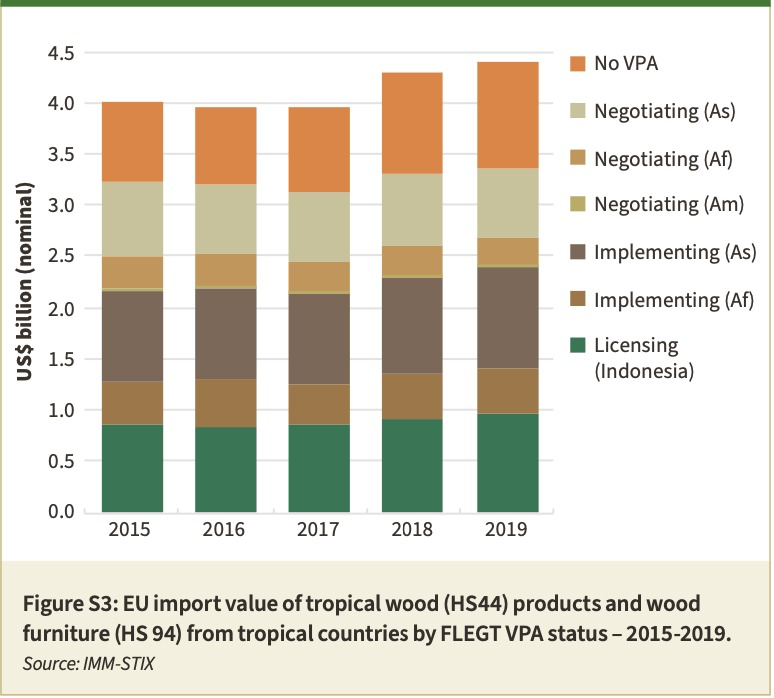

The total value of EU imports of tropical wood products (including direct imports and imports via third countries such as China)2 increased 1% in real terms to US$4.4 billion in 2019, following a 6% increase in 2018 (Figure S3). The increase in the total value of EU tropical wood product imports in 2019 was driven mainly by wood furniture with other smaller gains in imports of tropical sawnwood, ‘other’ (i.e. non-flooring) joinery, and other processed wood products. These gains offset a decline in imports of tropical panels/veneers, flooring and logs.

Tropical wood products’ share in total EU wood imports increased slightly, from 21.9% in 2018 to 22.8% in 2019, with countries engaged in the VPA process accounting for 76.1% of the total, down slightly from 76.7% the year before.

Summarising EU wood products imports from VPA partner countries other than Indonesia, none of which were issuing FLEGT Licences in 2019:

- the value of EU imports of wood products from the five African VPA implementing countries – Cameroon, Central African Republic (CAR), Republic of the Congo (RoC), Ghana, and Liberia – increased 3% to US$453 million in 2019 after rising 14% in 2018.

- the value of EU imports of wood products from Viet Nam, the only Asian VPA implementing country, increased 4% to US$976 million in 2019 after rising 5% in 2018.

- EU import value of wood products from Gabon, the Democratic Republic of the Congo, Côte d’Ivoire, the three VPA negotiating countries in Africa, declined 5.9% to US$283 million in 2019, following a rise of 1.3% in 2018.

- EU import value of wood products from Thailand, Lao PDR, and Malaysia, the three VPA negotiating countries in Asia, fell 3.7% to US$677 million in 2019.

- the value of EU imports of wood products from Guyana and Honduras, the two VPA negotiating countries in Latin America, fell 6%, to US$5 million in 2019, following a 13% increase in value in 2018.

EU imports of tropical wood products from non-VPA countries increased 5% to US$1.05 billion in 2019, building on a 17% gain in 2018. The increase was driven mainly by tropical hardwood plywood imported from China, tropical hardwood sawnwood and mouldings imported from Brazil, and wood furniture imported from India.

IMM surveys in 2019 flagged up that trade in VPA partner wood products – just like trade in many other commodities – was again facing an increasingly uncertain economic environment, both in the EU and globally. According to the EU Winter 2020 Economic Forecast published on 13 February 2020, GDP growth in the EU27 slipped to 1.5% in 2019, down from 2.1% in 2018. According to the UK Office of National Statistics, the UK economy grew by 1.4% in 2019, only marginally higher than the 1.3% rate in 2018, and recorded zero growth in the last quarter of the year.

Expanding range of IMM activities

With an expanding range of activities and outputs, IMM gained a thorough understanding of the relative market positions of FLEGT-licensed products from Indonesia, as well as timber and timber products from other VPA partner countries in the EU in 2019. The network of IMM correspondents continued to monitor market uptake of FLEGT Licences in the seven “key” EU countries3 accounting for the bulk (i.e. consistently around 90%) of EU tropical timber and timber product imports. IMM also continued to employ correspondents in Indonesia and Ghana. The two partner country correspondents produced update reports, used to inform the Indonesia section of this report and updates on Ghana on the IMM website, and acted as points of liaison between IMM and partner country authorities and organisations.

The EU trade survey conducted by IMM in 2019 had a broad scope, in terms both of content and target audience. The survey sample included EU importers of sawn timber, decking, plywood, mouldings logs, veneers, doors, window frames, as well as furniture andfurniture components and other wood products from VPA partner countries. Respondents accounted for up to 75% of the key EU countries’ total imports of HS Chapter 44 wood products. IMM correspondents also interviewed the FLEGT/EUTR Competent Authorities in their respective countries as well as timber trade federations and EUTR Monitoring Organisations.

In 2019, IMM published four special studies including on; architects’ attitudes to the use of tropical timber in construction and their awareness of the FLEGT VPA programme; EU public timber procurement policies; EU wood promotion programmes and their recognition of FLEGT; and the impact of FLEGT on forest sector investment. IMM also continued to organise “Trade Consultations”, which took place in Antwerp and Barcelona in 2019.

Also during 2019, IMM continued to build its statistical capacity so that it has access to, and can readily distribute, the latest global timber trade data each month. This now facilitates near real time monitoring, particularly important during the volatile trading conditions that have emerged since the onset of COVID-19. The insights gained from regular analysis of the latest trade statistics, surveys of traders and regulators, and special studies informs the series of IMM recommendations identified in this IMM Annual Report to help build market resilience for FLEGT- licensed timber in uncertain and challenging times.

Trade survey data on market perception of FLEGT-licensed timber

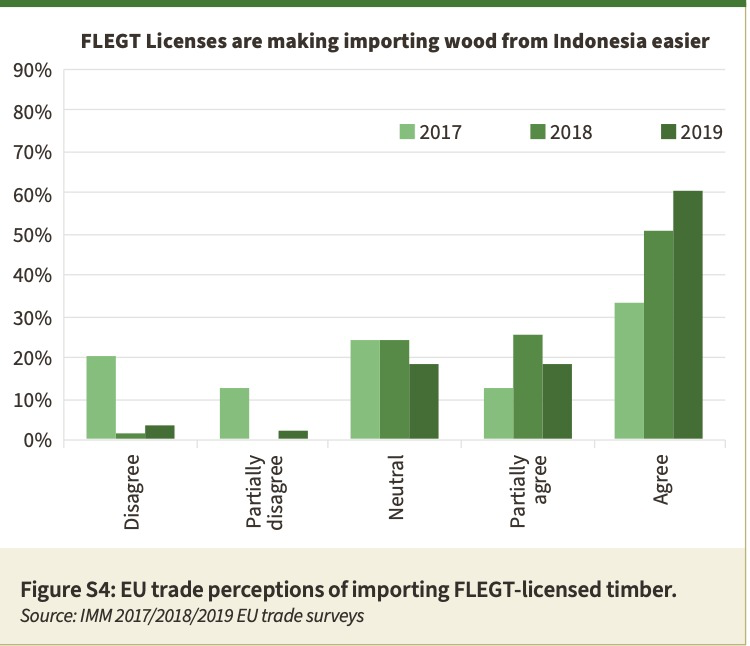

The 2019 IMM EU trade survey (chapter 8 of the Report) showed continuation of the positive trends in market perceptions of FLEGT-licensed timber from Indonesia. There was a sharp rise in the proportion of survey respondents finding the administrative process of importing FLEGT-licensed timber easily understandable and manageable between 2017 and 2019. Almost 80% of 2019 respondents said that FLEGT licensing was making importing wood products from Indonesia easier compared to EUTR due diligence (Figure S4). Moreover, a significantly higher number of respondents than in 2018 acknowledged sustainability aspects of FLEGT.

The 2019 trade survey confirmed contrasting impacts of FLEGT licensing and the EU Timber Regulation (EUTR) on European importers’ purchasing behaviour. 35% of respondents in 2018 and 38% in 2019 reported either small or big decreases in the share of tropical timber in their overall timber imports due to introduction of the EUTR. Survey respondents indicated that EUTR due diligence had narrowed their supply base in tropical countries. Respondents also indicated that the EUTR had caused the sector to reconsider its supply chain relationships, which had frequently resulted in increasing substitution of tropical hardwoods with alternatives, including temperate hardwoods, chemically or thermally modified timber or non-wood substitutes. No respondents in 2018 and just 2% of respondents in 2019 said their imports of tropical timber had increased as a result of the EUTR.

In the case of the market introduction of FLEGT-licensed timber from Indonesia, the majority of respondents – 87% (2018) and 83% (2019) – reported no change in the share of tropical timber in their overall timber imports. 13% of respondents in both years registered large or small increases.

The IMM Annual Report also provides an update on market constraints to FLEGT-licensed timber identified in the 2017 report (chapter 5 of the Report). The sharp decline in the number of both HS code and other FLEGT Licence mismatches (e.g. relating to shipments’ weight or volume) registered in 2018 has continued in 2019. There was also further progress in the development of an electronic licensing scheme, as well as in communication and marketing efforts, both within Indonesia and in the EU.

VPA partners in global tropical wood products trade

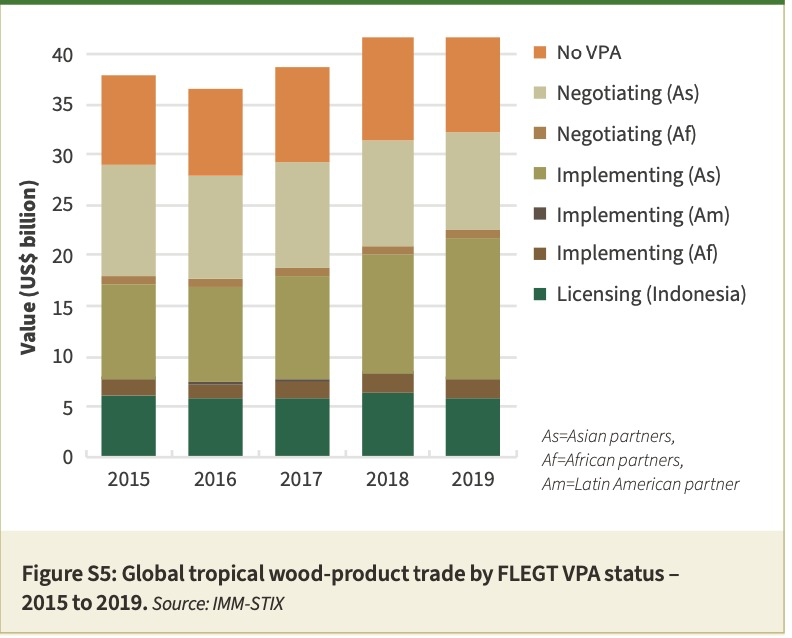

The IMM Annual Report includes an analysis of the share of VPA partner countries in global tropical wood products trade in 2019. This is to ensure that trade flows between VPA Partner countries and the EU are considered in their appropriate global context. Globally, trade in tropical wood products grew at a muchslower pace, by 0.2% to US$41.7bn, in 2019, than during the previous two years, when there was a sharp rebound from the dip in 2016, when the speculative rosewood boom in China had ended. Unlike the 2009 to 2014 period, when rapid trade growth was driven largely by China’s imports of primary wood products, particularly rosewood, recent growth is mainly due to rising wood furniture exports, notably from Viet Nam and India destined for the United States.

Global trade in tropical wood products in 2019 was influenced by overall cooling in the pace of economic growth. The global economy had already slowed sharply in the last three quarters of 2018, and global economic activity remained weak at least until the third quarter of 2019, according to the International Monetary Fund’s World Economic Outlook published on 15 October 2019. The IMF blamed this on “rising trade and geopolitical tensions”, which “have increased uncertainty about the future of the global trading system and international cooperation more generally, taking a toll on business confidence, investment decisions, and global trade”. Global economic growth was estimated at 2.9% in 2019 according to the World Economic Outlook from 9 January 2020. The trade dispute between the US and China had a direct impact on the trade in tropical wood products, increasing opportunities for South East Asian manufacturers, particularly in Viet Nam, in the US market for wood furniture and other finished wood products.

Summarising global trade in tropical wood products by VPA partners in 2019 (Figure S5):

- Exports of wood products from Indonesia fell 9% to US$5.93 billion in 2019, reversing gains made the previous year. Indonesia’s share of global trade in tropical wood products fell from 15.6% in 2018 to 14.2% in 2019. The EU accounted for 17.4% of Indonesia’s export value of wood products in 2019, up from 15.2% in 2018.

- Exports of wood products from Viet Nam were US$14.0 billion in 2019, a 19% increase comparedto the previous year. Viet Nam’s share of global trade in tropical wood products increased from 28.3% in 2018 to 33.5% in 2019. The EU accounted for 7.5% of Viet Nam’s export value of wood products in 2019, down from 8.6% in 2018.

- Exports of wood products from the five VPA implementing countries in Africa –Cameroon, Central African Republic (CAR), Republic of the Congo (RoC), Ghana, and Liberia – totalled US$1.69 billion in 2019, a 4% decrease from US$1.75 billion in 2018. These countries’ share of global trade in tropical wood products decreased from 4.2% in 2018 to 4.1% in 2019. The EU accounted for 26.8% of total export value of wood products by the five countries in 2019, up from 25.6% in 2018.

- In 2019, the three VPA negotiating countries in Asia – Thailand, Laos, and Malaysia – together exported US$9.4 billion of wood products, a 7% decline compared to 2018. Share of these countries in total global tropical wood product trade declined from 24.2% in 2018 to 22.5% in 2019. The EU accounted for 8.0% of total export value of wood products by the three countries in 2019, up from 7.7% in 2018.

- Total exports of wood products by the three VPA negotiating countries in Africa, Gabon,the Democratic Republic of the Congo, Côte d’Ivoire, increased 6% to US$886 million and accounted for 2.1% of global tropical trade in 2019, up from 2.0% in 2018. The EU accounted for 31.9% of total export value of wood products by the three countries in 2019, down from 36.5% in 2018.

- The two VPA negotiating countries in LatinAmerica, Guyana and Honduras, together exported US$115 million of wood products in 2019, a decline of 18% compared to the previous year. Their share of total tropical wood products trade fell from 0.34% in 2018 to 0.28% in 2019. The EU accounted for 4.6% of total export value of wood products from the two countries in 2019, up from 4.1% in 2018.

Requirements for legal timber in VPA partner export markets

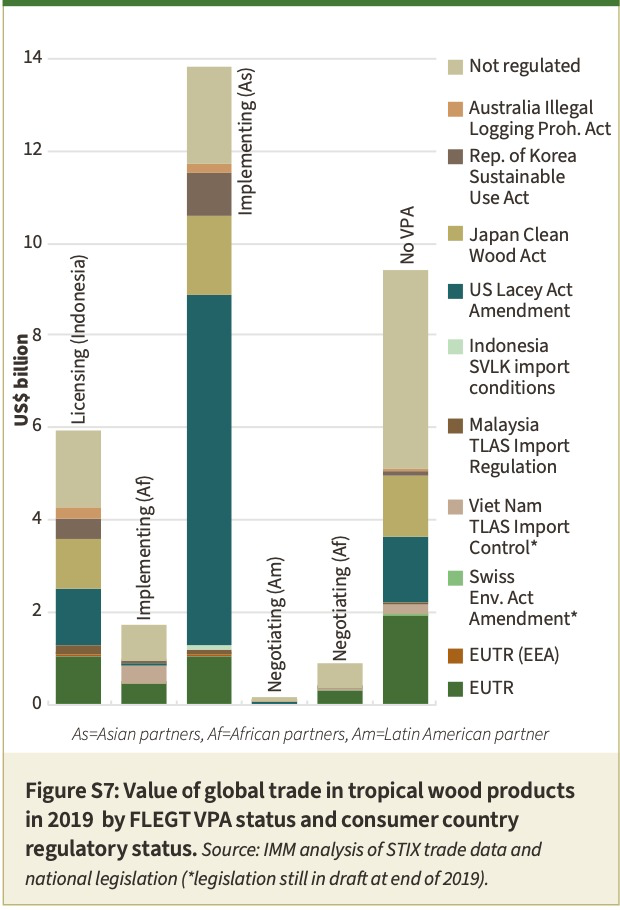

Alongside the assessment of the EU market for FLEGT- licensed timber and of global trade in tropical wood products, IMM monitors market impacts of policy measures and regulations with potential to generate demand for timber from FLEGT licensing VPA partner countries in non-EU countries. Analysis of trade data in 2019 shows that the goal of closing world markets to illegal wood products is already well advanced. In 2019, 66.5% (US$27.6 billion) of the total value (US$41.5 billion) of recorded tropical wood product exports worldwide were destined for countries with regulatory measures to eliminate illegal trade (Figure S6)4. This compares to 62.2% of tropical trade in 2018. The rise in the proportion of tropical wood products destined for regulated markets in 2019 was due primarily to the decline in imports by China, while US imports of wood products from tropical countries, particularly Viet Nam, increased sharply during the year.

The proportion of wood product exports destined for regulated countries was even higher for VPA partner countries. In 2019, 79% of all wood products exports by FLEGT licensing and VPA implementing countries was destined for regulated markets (Figure S7). In addition to the EU, which accounted for 12% of total exports by FLEGT licensing and VPA implementing countries in 2019, a large share of exports went to destinations regulated by the US Lacey Act (42%), Japan Clean Wood Act (13%), Republic of Korea Sustainable Use Act (7%) and Australian Illegal Logging Prohibition Act (2%). In 2019, the share of exports to regulated countries was particularly high for Indonesia (72%) and Viet Nam (85%). The share of exports to regulated markets was lower, but still significant, for VPA implementing countries in Africa (53%).

Conclusions

The IMM 2019 Annual Report shows an increasing level of recognition of FLEGT licensing as a means to reduce importers’ own risk under the EUTR and increasing awareness of the wider benefits of implementing FLEGT VPAs in partner countries. It also demonstrates EU trade familiarity with the administrative processes involved in importing FLEGT-licensed timber and a very high level of acceptance of these processes.

IMM survey data and feedback from IMM trade consultations suggests that EUTR has prompted EU importers to reassess their supply chains, especially in countries considered “high risk” and relationships were not unfrequently modified as a result (see Chapter 8 for details). However, this has not necessarily led to replacement ofnon FLEGT-licensed tropical timber suppliers with licensed. More frequently, importers reported that imports of certain products or species were discontinued and the product either sourced from specialist importers in the EU or replaced with non-tropical or even non-wood alternatives.

This highlights once more the fundamental importance of raising awareness of the long-term benefits of the sustainable use of tropical timber and addressing environmental prejudice in EU markets. Partner countries should be encouraged to develop individual marketing strategies for their prospective FLEGT- licensed timber products in the EU as they approach the end of the VPA implementation process.

It also highlights the importance of continuing efforts to bring more VPA processes to a successful conclusion and widen the source-base, range and availability of FLEGT- licensed timber and timber products.

The second IMM investment study, focussing on Viet Nam and Indonesia and summarised in this report, shows that FLEGT VPA implementation and licensing has a positive impact on the investment enabling environment in VPA partner countries. It identified correlation between the VPA, investment volumes and a shift in investments from forestry and logging towards investment in further processing industries in Indonesia. The study also demonstrates that the potential of the FLEGT VPA process for attracting additional investment would likely be reinforced by integration of relevant stakeholders from the banking and financial sector in the process.

Recommendations

The Report concludes with a series of recommendations.

- The second IMM investment study (summary in Chapter 11) found that VPAs can be a stimulating factor in the investment-enabling environment in the forest sector at several levels. FLEGT licensing should be promoted as a factor to improve the bank rating of forest sector enterprises in VPA countries and relevant actors should be included in the VPA processes.

- A 2019 IMM study of architects’ awareness and perceptions of FLEGT and tropical timber as a building material identified a low level of awareness of FLEGT itself, VPAs, FLEGT licensing and the EUTR. Professional bodies representing architects should be engaged to increase awareness of the FLEGT process. An important stakeholder group is daily making decisions on the choice of materials that has no understanding of the value and achievements of these processes. Many architectural bodies run continuing professional development courses for architects, and these offer an excellent opportunity to increase awareness of FLEGT processes.

- A second recommendation from the architects’ study is to engage with the World Green Building Council (WGBC) to raise awareness of the value of FLEGT licensing with a long-term goal of gaining credits for its use in WGBC affiliated programmes. Certified green building projects are set to increase and such programmes play a key role influencing material choices. Whilst some standards currently encourage the uptake of certified wood, only a small proportion allow solely FLEGT-licensed materials to be used. Only through recognition and credit within these standards will FLEGT licensing become of greater value to many projects and WGBC could play a pivotal role in raising awareness and increasing use of FLEGT within standards.

- Demonstrate the business benefits of the FLEGT licensing scheme in Indonesia to build trust. Indonesian furniture producers, in particular, see the licensing process as a bureaucratic hurdle rather than as a business opportunity. The current view is that it is not cost effective and any formerly promised market advantages are not tangible.

- Complete VPA implementation in other VPA countries as quickly as possible. All IMM surveys identified a clear message that FLEGT-licensed timber from a single country is insufficient.

- Encourage those companies not yet using FLEGT- licensed timber to do so. Awareness of EUTR varies among EU-based businesses, with awareness growing lower further down the supply chain. Some potential buyers of FLEGT-licensed timber are almost certainly unaware of it, what it stands for and what the benefits are for their businesses. Increased awareness at the business-to-business level would add value to the “brand” of FLEGT-licensed timber. Research undertaken in 2019 reinforces the view that EU-based companies will not re-source to Indonesia purely due to there being FLEGT-licensed material. Purchasing decisions are complex, and whilst easier compliance with the EUTR is a factor, it is not sufficiently important in its own right to drive a switch.

- The market recognition FLEGT-licensed products should be strengthened through branding and preferential treatment for licensed products, for example in public procurement.

- The private sector both in VPA Partner countries and in the EU needs to be actively engagedin the positive market development of FLEGT- licensed timber. Timber trade federations, for example, could play a leading role and have already started doing so in some countries. Environmental non-governmental organisations (ENGOs) that are open to supporting the FLEGT VPA process and commercial use of tropical timber should also be more actively engaged.

- IMM surveys demonstrate that the EUTR is having a significant impact on importers’purchasing behaviour in a number of key EU markets. However, continuing high import volumes in some Member States, e.g. from Brazil and Myanmar, which are under special observation by the FLEGT-EUTR Expert Group, indicate that harmonisation of due diligence standards across the EU should be further pursued. FLEGT licensing VPA partner countries could then potentially feel a stronger benefit of the “no-risk” status of FLEGT-licensed timber; however, other commercial and economic factors would still have to be taken into account.

Footnotes

1. In this report, wood, wood furniture, pulp and paper are referred to collectively as “timber and timber products”. Wood and wood furniture, when dealt with separately from pulp and paper, are referred to collectively as “wood products”.

2. Inline with previous IMM Annual Reports, this report focuses on tropical wood products as all current VPA partner countries are tropical and as a focus ontropical wood is stipulated in the IMM project However, care has been taken to place timber and timber products from VPA partner countries in awider trade context and to ensure that analysis takes account of all competitors, irrespective of whether tropical or non-tropical. Tropical wood products are defined in this report as:

- all productsin HS 44 and wood furniture products in HS 94 exported by countries located predominantly in the tropics, except Brazil and Mexico (where exports are known from analysis of trade reports and flows over numerous years to be dominated by products manufactured from plantations outside the tropical zone);

- all productsfrom Brazil identified specifically as “hardwoods” (but excluding eucalyptus) in HS 44 (since feedback from regular trade contacts indicate theseare predominantly of tropical species);

- and allproducts identified specifically as “tropical hardwoods” from all other countries (tropical hardwoods can be reliably identified in trade statistics for logs,sawnwood, plywood and veneers).

This definition of “tropical wood products” creates some inconsistencies – notably in relation to Viet Nam where a significant, but unknown, proportion of HS44 and 94 products are composed of non-tropical timber, and Brazil, where all HS94 wood furniture is excluded because there is no way to differentiate tropical from non-tropical, or hardwoods from softwoods, in this product category. However, overall it is believed to represent a reasonable compromise capturing, atglobal scale, the vast majority of products more likely manufactured from tropical wood, while excluding the vast majority of products more likely to be manufactured from non-tropical woods.

3. Belgium,France, Germany, Italy, Netherlands, Spain, UK

4. In addition to the EU (inclusive of the UK), IMM identified the following 10 countries as “regulated markets” in 2019: Australia, Iceland, Lichtenstein, Norway,Indonesia, Japan, Malaysia, Republic of Korea, Switzerland, and US.