The impact of FLEGT VPAs on forest sector investment risk in Indonesia and Viet Nam

DOWNLOADS

CATEGORY

Special Study

PUBLISHED DATE

December 2020

AUTHORS

Christian Held, UNIQUE forestry and land use

EDITORS

Sarah Storck

DESCRIPTION

The impact of FLEGT VPAs on forest sector investment risk in Indonesia and Viet Nam

KEY FINDINGS

MM commissioned a follow-up study of FLEGT impact on forest sector investment, the investment enabling environment and forest sector resilience to economic crisis in Indonesia. Viet Nam was also included in the study as well for the following reasons:

- Viet Nam is a regional competitor to Indonesia in the wood and forest products sector and a key processing hub.

- Availability and quality of investment data allows for monitoring of investment activity in Viet Nam over a relevant period of time.

For both countries, most recent time series of forest sector investment data was retrieved from the Systems of National Accounts. The historical fluctuations of forest sector investments were contrasted against the VPA negotiation and implementation process in each country.

To contextualize and add qualitative aspects to the statistical investment data, interviews with medium and large sized enterprises were conducted in July and August 2020 in each country. In addition, a set of interviews with institutional actors from sector associations, civil society and relevant ministries was conducted.

Due to the limited number of interviews, the results of this study cannot necessarily be considered representative of the entire forest sector in the two countries. However, the information presented has been validated and approved by forest sector experts from Indonesia and Viet Nam.

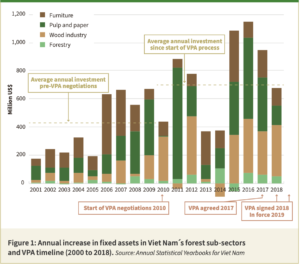

Key outcomes Viet Nam

- Comparison of the time periods before and after the start of VPA negotiations in 2010 shows a significant increase in average investment volumes per year after 2010. The average annual investment volume in the forest sector increased from US$415 million pre-2010 to US$690 million after VPA negotiations started.

- However, survey respondents did not mention that the VPA negotiations had influenced their investment decisions. They attributed the increase in forest sector investment in the period after 2010 to important reforms of the economic system in Viet Nam, especially the WTO membership (2007) and subsequent government resolutions to reforming the investment enabling environment in 2010 and in 2011.

- For the VPA implementation period post-2019, survey respondents expect that the Timber Legality Assurance System (TLAS) will substantially improve transparency in timber trade, including imports, exports and domestic trade flows.

- The enterprises primarily perceived the VPA asan instrument to provide proof of the legal and sustainable origin of wood products and thus secure improved access to regulated markets.

- Further, Vietnamese enterprises saw potential for the operational VPA in the post-2020 period in terms of market risk mitigation and capital mobilization.

- The enterprises emphasized that accelerating the implementation of the TLAS to cover the entire forest sector is crucial to ensure international credibility and reputation of Vietnamese wood products exports in the EU and other regulated markets.

- In light of the CoViD-19 pandemic, the VPA is expected to have a stabilizing effect on Vietnamese export market shares in regulated markets.

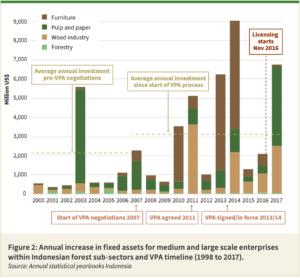

Key outcomes Indonesia

- Average annual forest sector investment almost doubled in the decade after the beginning of VPA negotiations (2007 to 2017) to reach US$3.1bn per annum. Between 1998 and 2006 forest sector investment was US$1.7 billion per annum.

- After 2010, the year when the VPA was agreed, the focus of investment has shifted from pulp and paper towards wood processing and furniture manufacturing.

- Survey respondents partly attributed the increase in investment in the wood and furniture sectors to improvements related to the FLEGT VPA process. These included improved Indonesian market access to regulated markets and substantial improvements in forest sector governance.

- Companies perceived positive impacts of the VPA on mitigating the economic effects of the CoViD-19 crisis by avoiding illegal logging and maintaining access to regulated markets for the post-crisis phase.

- With a view to post-crisis recovery, a key message from respondents was the need to boost export sales and intensify marketing efforts for Indonesian wood products. A number of respondents voiced dissatisfaction with EU efforts to “promote a favorable position” of products covered by the VPA in the EU market and felt that more needed to be done in the EU to comply with Article 13 of the VPA, which addresses this topic.

Conclusions

The 2019 baseline study demonstrated that a FLEGT VPA alone cannot compensate for the lack of market drivers, such as an investment friendly environment, efficient production systems and favourable cost situation, among many other factors. However, the 2020 study indicates that in countries where all or some of the above criteria are met, as is the case in Viet Nam and Indonesia, VPAs can improve the investment enabling environment in the forest sector by:

- Creating improved access to regulated markets;

- Improving access to capital and investors through the formalization of forest sector enterprises;

- Eliminating market distortions through illegal competition;

- Establishing good forest governance, addressing social and environmental risk factors;

- Ensuring long term viability of operations by enhancing sustainable forest management practices.

To further strengthen the positive impacts of VPAs on forest sector investment, the following aspects should be considered:

- Expanding demand from regulated markets (i.e. support the development of timber legislation in additional countries, for example China or India);

- Strengthening the market position of FLEGT licensed products through improved marketing efforts and preferential treatment (e.g. in public procurement);

- Promoting FLEGT licensing as a factor to improve the credit rating of forest sector enterprises in VPA countries;

- Ensuring formalization of all market participants once a VPA is signed and implemented;

- Minimising additional costs for producers, for example by developing digital solutions for documentation and monitoring;

- Ensuring that no shortages of regulated timber occur due to limitations for implementing the Timber Legality Assurance Systems (i.e. technical and personal resources to operate the system).

MM commissioned a follow-up study of FLEGT impact on forest sector investment, the investment enabling environment and forest sector resilience to economic crisis in Indonesia. Viet Nam was also included in the study as well for the following reasons:

- Viet Nam is a regional competitor to Indonesia in the wood and forest products sector and a key processing hub.

- Availability and quality of investment data allows for monitoring of investment activity in Viet Nam over a relevant period of time.

For both countries, most recent time series of forest sector investment data was retrieved from the Systems of National Accounts. The historical fluctuations of forest sector investments were contrasted against the VPA negotiation and implementation process in each country.

To contextualize and add qualitative aspects to the statistical investment data, interviews with medium and large sized enterprises were conducted in July and August 2020 in each country. In addition, a set of interviews with institutional actors from sector associations, civil society and relevant ministries was conducted.

Due to the limited number of interviews, the results of this study cannot necessarily be considered representative of the entire forest sector in the two countries. However, the information presented has been validated and approved by forest sector experts from Indonesia and Viet Nam.

Key outcomes Viet Nam

- Comparison of the time periods before and after the start of VPA negotiations in 2010 shows a significant increase in average investment volumes per year after 2010. The average annual investment volume in the forest sector increased from US$415 million pre-2010 to US$690 million after VPA negotiations started.

- However, survey respondents did not mention that the VPA negotiations had influenced their investment decisions. They attributed the increase in forest sector investment in the period after 2010 to important reforms of the economic system in Viet Nam, especially the WTO membership (2007) and subsequent government resolutions to reforming the investment enabling environment in 2010 and in 2011.

- For the VPA implementation period post-2019, survey respondents expect that the Timber Legality Assurance System (TLAS) will substantially improve transparency in timber trade, including imports, exports and domestic trade flows.

- The enterprises primarily perceived the VPA asan instrument to provide proof of the legal and sustainable origin of wood products and thus secure improved access to regulated markets.

- Further, Vietnamese enterprises saw potential for the operational VPA in the post-2020 period in terms of market risk mitigation and capital mobilization.

- The enterprises emphasized that accelerating the implementation of the TLAS to cover the entire forest sector is crucial to ensure international credibility and reputation of Vietnamese wood products exports in the EU and other regulated markets.

- In light of the CoViD-19 pandemic, the VPA is expected to have a stabilizing effect on Vietnamese export market shares in regulated markets.

Key outcomes Indonesia

- Average annual forest sector investment almost doubled in the decade after the beginning of VPA negotiations (2007 to 2017) to reach US$3.1bn per annum. Between 1998 and 2006 forest sector investment was US$1.7 billion per annum.

- After 2010, the year when the VPA was agreed, the focus of investment has shifted from pulp and paper towards wood processing and furniture manufacturing.

- Survey respondents partly attributed the increase in investment in the wood and furniture sectors to improvements related to the FLEGT VPA process. These included improved Indonesian market access to regulated markets and substantial improvements in forest sector governance.

- Companies perceived positive impacts of the VPA on mitigating the economic effects of the CoViD-19 crisis by avoiding illegal logging and maintaining access to regulated markets for the post-crisis phase.

- With a view to post-crisis recovery, a key message from respondents was the need to boost export sales and intensify marketing efforts for Indonesian wood products. A number of respondents voiced dissatisfaction with EU efforts to “promote a favorable position” of products covered by the VPA in the EU market and felt that more needed to be done in the EU to comply with Article 13 of the VPA, which addresses this topic.

Conclusions

The 2019 baseline study demonstrated that a FLEGT VPA alone cannot compensate for the lack of market drivers, such as an investment friendly environment, efficient production systems and favourable cost situation, among many other factors. However, the 2020 study indicates that in countries where all or some of the above criteria are met, as is the case in Viet Nam and Indonesia, VPAs can improve the investment enabling environment in the forest sector by:

- Creating improved access to regulated markets;

- Improving access to capital and investors through the formalization of forest sector enterprises;

- Eliminating market distortions through illegal competition;

- Establishing good forest governance, addressing social and environmental risk factors;

- Ensuring long term viability of operations by enhancing sustainable forest management practices.

To further strengthen the positive impacts of VPAs on forest sector investment, the following aspects should be considered:

- Expanding demand from regulated markets (i.e. support the development of timber legislation in additional countries, for example China or India);

- Strengthening the market position of FLEGT licensed products through improved marketing efforts and preferential treatment (e.g. in public procurement);

- Promoting FLEGT licensing as a factor to improve the credit rating of forest sector enterprises in VPA countries;

- Ensuring formalization of all market participants once a VPA is signed and implemented;

- Minimising additional costs for producers, for example by developing digital solutions for documentation and monitoring;

- Ensuring that no shortages of regulated timber occur due to limitations for implementing the Timber Legality Assurance Systems (i.e. technical and personal resources to operate the system).