Market News

EU-Indonesia first half 2022 trade trends

Global export value of Indonesian timber and paper product grows 10% year-on-year Indonesia’s...

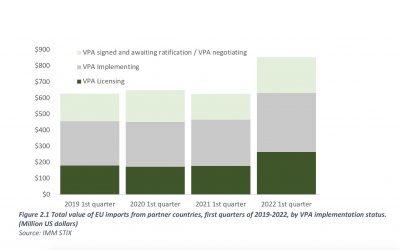

EU-VPA partner country trade overview – first half of 2022

In the first half of 2022 EU imports of timber and wood products from VPA partner countries grew...

EU tropical Timber market trends 2022

More market mayhem The situation in key EU sales markets for tropical timber and timber...

Policy News

Jakarta consultation highlights usefulness of IMM data

Representatives from Indonesian government agencies, Civil Society Organisations, and the private...

EU’s deforestation-free regulatory proposal raises concerns about impacts on FLEGT VPAs

Peatland forest in Parupuk village, Katingan. Central Kalimantan. Credit: CIFOR The ITTO Market...

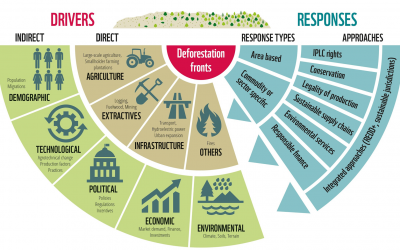

Different takes on deforestation regulation

Drivers of deforestation. Image by WWF. With market import controls to combat deforestation...

IMM Project News

FLEGT awareness raising key, say Ghana consultations

With the qualification that it could be better disseminated, Ghana timber sector stakeholders rate...

Nantes consultation backs ongoing FLEGT and tropical trade market monitoring

The consensus of the Independent Market Monitor’s (IMM) recent stakeholder consultation in France...

Indonesian FLEGT Licences: EU survey indicates high level of awareness and satisfaction with administrative procedures

The 2021 IMM EU trade survey demonstrates that, after five years of FLEGT licensing, the level of...

Newsletters

| ISSUE | DOWNLOAD |

| IMM Summary Newsletter H2/2020 | English | Bahasa Indonesia | Français |

| IMM Summary Newsletter H2/2019 | English |Bahasa Indonesia | Français |

| IMM Summary Newsletter H1 / 2019 | English |

| IMM Summer 2019 Newsletter | Bahasa Indonesia |

| IMM Spring 2019 Newsletter | Bahasa Indonesia |

| IMM Autumn 2018 Newsletter | English | Français |

| IMM Summer 2018 Newsletter | English | Français |

| IMM Spring 2018 Newsletter | English | Français |

| IMM Autumn 2017 Newsletter | English |