The economic background in the EU created challenging market conditions for timber products from VPA partner countries between 2014 and 2016. VPA partner exporters had to contend with the relative weakness of the euro and other European currencies, the slow pace of EU economic recovery from the financial crises, the dominant position of European and Chinese manufacturers in many market segments, the strong fashion for temperate woods (particularly oak), intense and rising competition from a wide range of non-wood substitutes, and uncertainty created by the Brexit vote in June 2016.

Key economic sectors in the EU were recovering only slowly during the review period. Europe’s construction sector was under-performing compared to other industrial sectors and becoming more focused on new build and Eastern Europe, sectors generally less attractive as markets for tropical wood than refurbishment in western Europe. Overall growth in the furniture sector was very slow; by the end of 2016, the total volume of furniture manufacturing in Europe was still down around 15% compared to the period before the global financial crises.

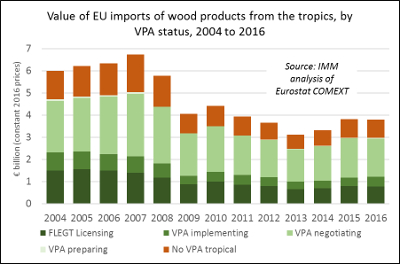

Share of tropical wood in EU imports

Measured in euros, the value of EU imports of tropical wood products increased 15% to €3.82 billion in 2015 before declining 1% to €3.79 billion in 2016. The euro value trend was influenced by exchange rate swings, particularly a 20% depreciation against the US dollar between July 2014 and March 2015. In US dollar terms, EU imports of tropical wood products were flat at a historically low level of around $4 billion per year in the period 2014 to 2016.

The share of tropical countries in total EU wood product import value fell continuously from 35% in 2004 to a low of 21% in 2014. Tropical countries lost share initially to China in the period 2004 to 2010, and then to North American, Russian and non-EU European countries in the period 2011 to 2014.

However tropical countries regained a little share in import value mainly at the expense of Russia and non-EU European countries in 2015 and of China in 2016. The recovery in EU imports of tropical wood products in 2015 and 2016 was particularly pronounced for furniture and sawn wood, although there were minor gains for all other product groups.

During the review period, the euro exchange rate was generally unfavourable to Asian suppliers, being low against the US dollar but strong against currencies in Eastern European countries including Russia and Ukraine which both significantly increased hardwood supply to the EU. African countries benefitted to some extent in the EU market, but main beneficiaries were domestic and Eastern European manufacturers.

EU imports of wood products from Indonesia, measured in euros, increased 16% to €796 million in 2015 and then declined 2% to €781 million in 2016. Indonesia’s share of total EU tropical wood-product imports remained unchanged at 21% between 2013 and 2016.

EU imports of wood products from the five African VPA implementing countries increased 12% to €377 million in 2015 and then an additional 13% to €426 million in 2016. As a group, the share of African VPA implementing countries in total EU tropical wood import value declined from 11% to 10% between 2013 and 2015 but rebounded to 11% in 2016 due mainly to a surge in imports from Cameroon.

Rising competition from domestic manufacturers

In most EU market segments, domestic producers are the major competitors to wood product suppliers in VPA partner countries. Of total supply into the EU market in 2015, domestic producers accounted for 97% of sawlogs and veneer logs, 82% of sawn hardwood, 88% of veneer, 53% of plywood, 99% of wood windows, 95% of wooden doors, 70% of real-wood flooring and 87% of wood furniture.

During the review period, the share of EU wood manufacturers in most market sectors was rising, boosted by the relative weakness of the euro and the market advantages of proximity to the consumer. One indicator of the improved global competitiveness of domestic manufacturers is the EU’s trade surplus in wood products. After 6 years of continuous increase, the value of EU exports of wood products peaked at €20.51 billion in 2015, the highest level ever, and fell by only 0.5% to €20.40 billion in 2016. In 2016, the EU had a €3 billion trade surplus in wood products; this compares to a €3 billion deficit before the financial crises

Even in those wood sectors where European manufacturers have traditionally been weak and more dependent on imports, such as durable goods for outdoor use and in appearance grade wood, new innovative products are taking share from external suppliers. Key innovations include a wide range of new surface finishes to enhance the appearance and performance of temperate woods and panel products, and thermal and chemical modification processes to enhance the durability of domestic wood species.

Implications of trend towards engineered wood products

A key trend in the EU creating significant challenges, and a few new opportunities, for wood products suppliers in VPA partner countries is growing demand for engineered wood products (EWPs) in a wide range of wood applications. The trend is closely linked to the move to rising quality and efficiency standards in the EU and to more modular forms of off-site, prefabricated construction.

EWPs tend to offer higher dimensional stability and greater strength than solid timber products, allowing more precise engineering which in turn improves product performance and longevity. They also help increase material efficiency, allowing lower grade and smaller dimension wood to be converted into high-performance components.

The move to EWPs has been challenging for external suppliers into the EU, particularly in the tropics, and EWP markets are heavily dominated by domestic manufacturers that are familiar with the required technical standards and well positioned to work closely with building engineers, architects and contractors.

Although VPA partners in South East Asia are supplying various forms of glulam into the EU market, and possibly also LVL, this is currently restricted to non-structural applications. However, there may be some limited new opportunities to supply tropical wood for specialist grades of EWP drawing on the high strength to weight ratio and durability of tropical wood.